Mental health conversations are no longer hidden behind closed doors. Over the last few years, more people have started speaking openly about stress, anxiety, burnout, depression, and emotional exhaustion. From college students and working professionals to parents and senior citizens, mental health challenges are affecting almost every age group. But while awareness has improved, one major concern still remains unresolved — affordability.

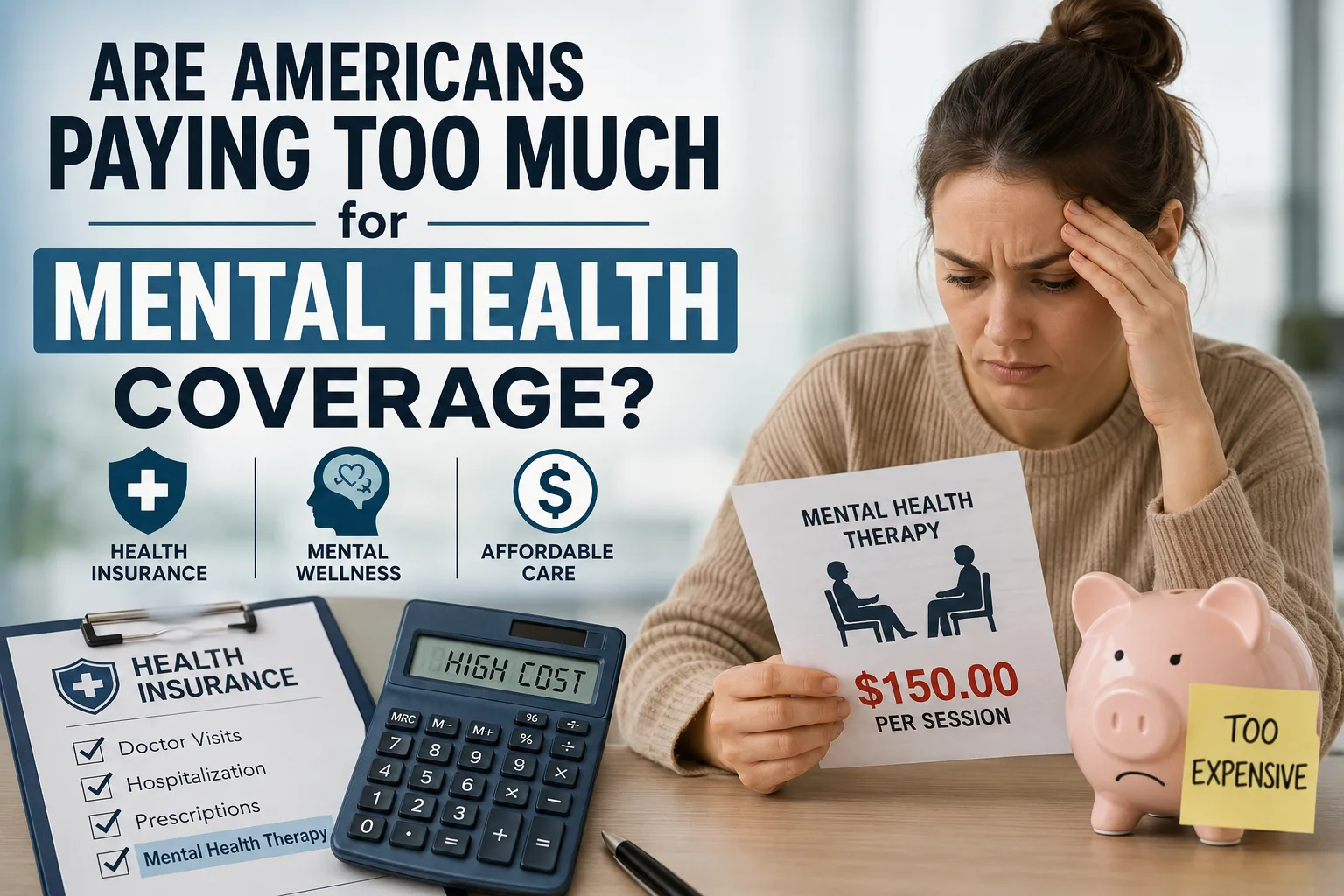

Many families are now questioning whether emotional wellness has quietly become a luxury. Therapy sessions, counseling appointments, prescription medications, and insurance premiums can quickly create financial pressure. In fact, one of the biggest concerns people search online today is does health insurance cover therapy because many individuals still do not fully understand what their plans actually include. Some insurance providers cover only limited sessions, while others require high co-pays or approvals before treatment even begins. As a result, many people delay getting help simply because they are worried about the cost.

Why Mental Health Costs Feel More Visible Today

A decade ago, mental health treatment was often considered optional by many households. Today, the situation looks very different. Long working hours, social media pressure, financial uncertainty, and post-pandemic lifestyle changes have pushed emotional wellness into everyday conversations. More people are recognizing the signs of burnout and emotional fatigue, which naturally increases demand for professional support.

However, increased awareness has also exposed another issue. Even insured individuals often discover hidden expenses when they finally decide to seek therapy or counseling. Some plans only include network-approved therapists, while others limit how many appointments are covered annually. This creates confusion and frustration, especially for people already dealing with emotional stress.

The Emotional Price of Delaying Treatment

When mental health support becomes expensive, many people choose to wait. They convince themselves that stress will eventually disappear or that things are “not serious enough” for professional help. Unfortunately, untreated emotional struggles rarely improve on their own.

A person struggling with anxiety may begin avoiding social situations or work responsibilities. Someone dealing with depression might lose motivation, relationships, or even career opportunities. Over time, small emotional issues can slowly turn into long-term mental health conditions that require even more expensive treatment later.

This financial hesitation creates a dangerous cycle. People avoid therapy because it costs too much, but delaying treatment often leads to larger emotional and medical expenses in the future. In many ways, the true cost of mental health care is not just financial — it is deeply personal.

Insurance Plans Are Becoming More Complicated

Health insurance was originally designed to reduce financial stress during medical emergencies. But modern plans often feel difficult to understand, especially when mental health benefits are involved. Coverage rules, exclusions, waiting periods, deductibles, and provider networks can confuse even educated consumers.

Many people also wonder how much is health insurance per month before selecting a plan that includes mental health support. The answer varies widely depending on age, location, coverage type, and employer contributions. Lower monthly premiums may look attractive initially, but these plans sometimes offer weaker mental health benefits or higher out-of-pocket expenses later. On the other hand, comprehensive plans with strong therapy coverage can feel financially overwhelming for middle-class families trying to manage monthly budgets.

This situation leaves consumers stuck between affordability and quality care. Some choose cheaper plans and sacrifice mental wellness support, while others pay higher premiums hoping to avoid future healthcare expenses.

Employers Are Slowly Changing Their Approach

Interestingly, workplaces have started paying more attention to employee mental health than ever before. Companies now understand that emotional wellness directly affects productivity, creativity, and retention. Burnout employees are more likely to leave jobs, take sick leave, or struggle with performance.

As a result, many organizations are adding therapy apps, counseling sessions, and wellness programs into employee insurance packages. While this is a positive shift, the quality of these benefits still varies significantly between employers. Large corporations often provide stronger mental health coverage compared to smaller businesses with limited budgets.

For freelancers, self-employed professionals, and gig workers, the challenge becomes even harder. Without employer-sponsored insurance, many people must purchase individual plans that may not fully support ongoing therapy or psychiatric treatment.

The Social Impact of Expensive Mental Healthcare

Mental healthcare costs do not affect only individuals. Entire families experience the emotional and financial pressure together. Parents may postpone their own therapy to prioritize children’s education expenses. Young adults may avoid counseling because they fear becoming a financial burden on their families.

In communities where mental health stigma still exists, expensive treatment creates another barrier. People may already feel hesitant to seek support, and high costs only reinforce the idea that therapy is unnecessary or inaccessible. This can quietly increase emotional isolation across society.

The problem becomes even more concerning in rural or underserved areas where mental health professionals are limited. In such places, people may travel long distances for appointments while still paying expensive consultation fees. Insurance coverage alone does not solve accessibility issues if healthcare infrastructure itself remains uneven.

Why Transparency Matters More Than Ever

One of the biggest frustrations consumers face is the lack of transparency around healthcare costs. Many patients do not know what services are covered until they receive unexpected bills. Therapy sessions may appear affordable initially, only for patients to later discover claim limitations or denied coverage.

Clear communication from insurance companies could reduce much of this confusion. People deserve simple explanations about therapy benefits, session limits, prescription coverage, and emergency mental health support before choosing a plan. Transparent pricing would allow families to make smarter financial decisions instead of guessing future medical expenses.

At the same time, consumers also need to carefully review insurance policies rather than focusing only on premium costs. Mental health coverage is no longer a secondary feature. For many households, it has become just as important as emergency hospitalization benefits.

The Future of Mental Health Coverage

The conversation around mental health is changing rapidly, and insurance systems are slowly trying to adapt. Governments, employers, healthcare providers, and insurance companies all face growing pressure to make emotional wellness support more affordable and accessible. As awareness increases, consumers are becoming more informed about their rights and healthcare choices.

This is especially important during open enrollment for health insurance, when individuals and families compare plans for the upcoming year. More people are now paying attention to therapy coverage, counseling benefits, and mental healthcare networks before making final decisions. That shift itself shows how priorities are changing.

Mental health should not feel like a privilege reserved only for those who can afford expensive plans. Emotional well-being affects careers, relationships, physical health, and overall quality of life. If healthcare systems truly aim to support people, then mental wellness coverage must become simpler, clearer, and more affordable for everyone.