A CD interest calculator is essential for investors as it helps them plan accurately regarding their investment earnings in a certificate of deposit. Unlike savings accounts, CDs require fixed interest payments for a given period, which requires careful consideration.

Why Accuracy Matters in CD Interest Calculator

- Fixed-Term Nature: CDs lock your money for specific periods (3 months to 5 years)

- Early Withdrawal Penalties: The majority of the banks levy a great fee if the money is withdrawn before the time

- Interest Rate Changes: changes over the period and make APY (Annual Percentage Yield) vary from one term to another.

- Compounding Effects: Changing the compounding frequency significantly impacts the return end.

Elevate Your Saving Strategy with the CD Interest Calculator

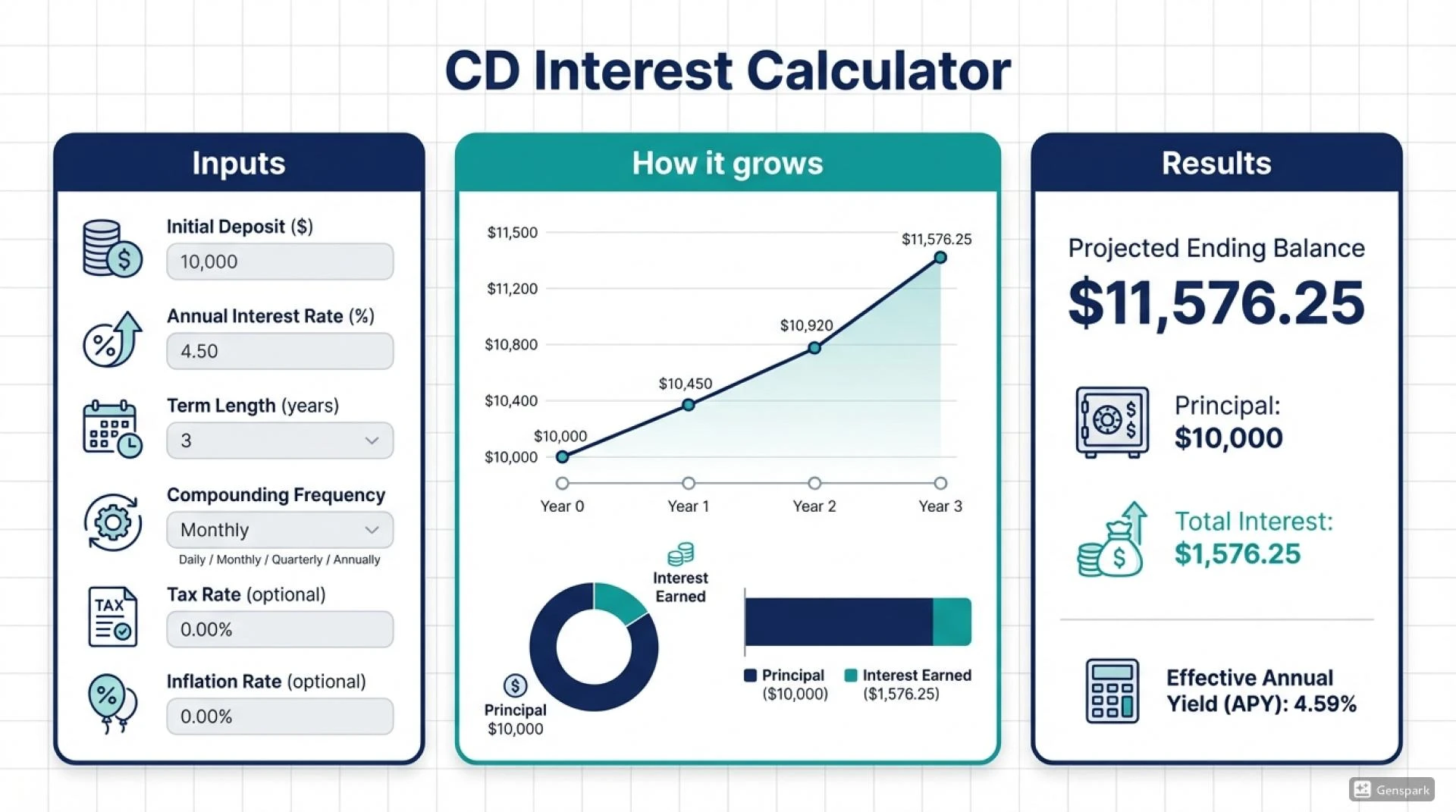

Knowing how money multiplies is vital to any solid financial strategy. A CD interest calculator makes this journey easier. With this simple device, you can estimate the value of your certificate of deposit (CD), putting you in control to settle on a plan that matches your objective.This section serves as your demystified guide to the CD interest calculator. Every feature within is put in place to streamline your experience. More about CD Interest Calculator

1. Principal Amount

Here, indicate the amount you expect to invest in the CD. The system is set to accept whole pound representation. If, for example, you wish to place a £5,000 investment, write “5000”.

2. Interest Rate

Your payment rate is linked to the specified investment fraction percent cited prior. This value is often cited as the annual percentage yield (APY) with your credit union. Type here the value of the interest rate you expect. For instance, if the interest cost is supposed to be 2.5 percent, type “2.5”.

3. Compounding Frequency

Compounding frequency dictates how frequently the accrued Interest is added to your principal, allowing you to earn additional Interest. This option includes:

- Annually: Interest is calculated and added one time per year.

- Semiannually: Interest is calculated and added two times each year.

- Quarterly: Interest is calculated and added to the account four times yearly.

- Monthly: Interest is calculated and added every month, resulting in twelve additions yearly.

In this case, select the compounding frequency applicable to the specific CD that you are considering.

4. Time Period (Term Length)

The time period or the term length indicates the extent of time your money will be held in the CD. This figure is most often represented by year. For the term of the CD, indicate the number of years. Take the example of a 3-year CD; you would enter “3”.

5. Calculate Button

After accurately inputting the principal amount, interest rate, compounding frequency, and period, click the “Calculate” Button. The CD interest calculator will now process your data.

6. Results Display

With this calculator, you will obtain around this estimated result:

- Total Interest Earned: The total amount of Interest accrued on the CD is the total Interest earned.

- Total Value at Maturity: Represents the total of the initial principal sum and the Interest earned on it.

Practical Scenario That Will Help You Make Decision

Let’s analyze a few cases where a CD interest rate calculator can assist decision-making.

Example 1: Evaluating Short Term Choice

For instance, imagine you have £10,000 to invest and are looking at two 1-year CDs:

- CD A: Has an interest rate of 3 percent per annum with monthly compounding.

- CD B: Has an interest rate of 3.1 percent per annum with annual compounding.

- Through the CD interest Calculator feature of the calculator, you can input:

- CD A: Principal: £10000, Interest Rate: 3, Compounding Frequency: Monthly, Period: 1. With the calculator, total Interest earned will exceed £300 because of the monthly compounding effect.

- CD B: Principal: £10000, Interest Rate: 3.1, Compounding Frequency: Annually, Time Period: 1. This calculator shows a total interest earned of £310.

In this case, the assumption is valid where, for a 1-year term, a lower compounding rate yields a higher return than a higher rate.