In the modern era, we are more "educated" than ever before. We produce millions of specialized professionals like engineers, doctors, and lawyers who have mastered complex technical skills. Yet, a peculiar paradox persists: many of these highly intelligent individuals live paycheck to paycheck, trapped in a cycle of financial stress.

This disconnect suggests a fundamental flaw at the intersection of Education and Psychology. While our schools are excellent at teaching us how to work for money, they remain silent on how to make money work for us.

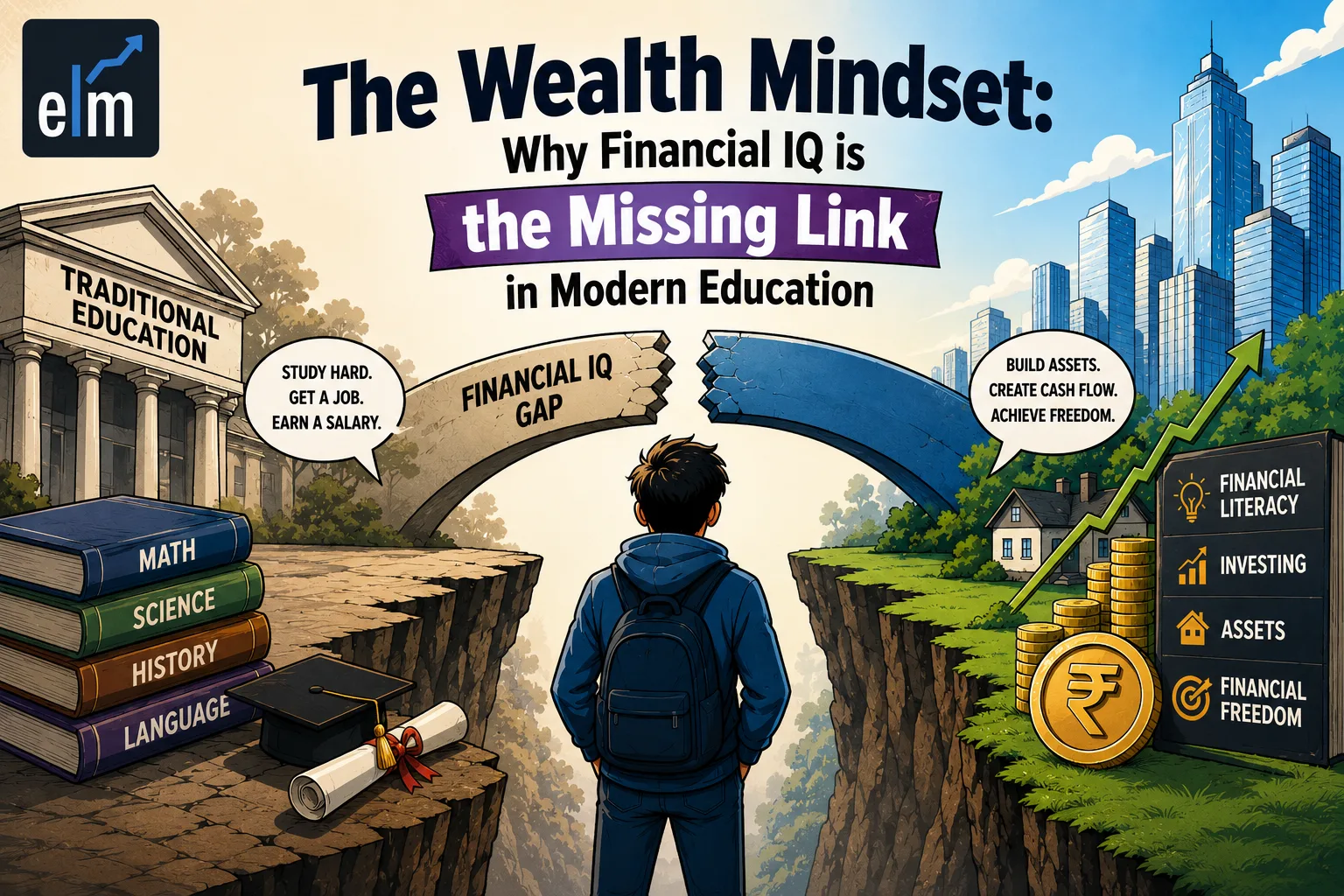

1. The Financial IQ Gap: What Schools Still Aren't Teaching

The traditional schooling system was designed during the Industrial Age to create a reliable workforce. Consequently, the curriculum focuses on building professional skills but almost entirely ignores Financial IQ.

According to the lessons in Rich Dad Poor Dad, the "Smart Dad" or "Poor Dad" mindset encourages children to study hard to find a stable job in a good company. While this provides security, it lacks the financial literacy required to build lasting wealth.

Why Professional Success Doesn't Equal Financial Success

Most graduates enter the workforce without understanding the difference between an asset and a liability. They are taught to:

- Write impressive resumes rather than financial plans.

- Work for a salary rather than building business systems.

- View their primary residence as an asset, when it often functions as their largest liability.

- Cash Flow vs. Capital Gains: High-IQ investors focus on cash flow (money coming in regularly) rather than just capital gains (waiting for an asset's price to go up). While the average person buys a stock hoping it will rise, a wealthy mindset seeks assets like rental properties or dividend stocks that pay them to own them.

- The Debt Lever: Understanding the difference between "Bad Debt" (consumer credit used for lifestyle) and "Good Debt" (loans used to acquire income-producing assets).

Without a foundation in financial literacy, individuals become dependent on their employers. This creates a "Rat Race" where every increase in income is immediately met by an increase in expenses and taxes, leaving the individual exactly where they started.

2. Overcoming Financial Cynicism: Moving Past the Fear of Losing

The biggest barrier to financial independence isn't a lack of opportunity; it’s the psychology of fear. Most people stay in the Rat Race because they are driven by two primary emotions: Fear and Greed.

The Anatomy of Financial Fear

We are conditioned to believe that mistakes are "bad." In school, making a mistake leads to a lower grade. In the real world, however, failure is the greatest teacher.

Financial cynicism often manifests as:

- The Fear of Losing Money: This leads people to "play it safe," which often results in missing out on the greatest periods of wealth creation.

- Criticism Over Analysis: Cynics tend to criticize new investment opportunities (like the stock market or real estate) as "risky" without performing a meaningful analysis to understand the mechanics of the risk.

- Managing Risk vs. Avoiding Risk: Financial IQ isn't about being "reckless"; it’s about calculating the "asymmetric risk-reward." This means looking for opportunities where the potential downside is capped and known, but the upside is significant.

- Hedging: Learning how to use insurance or diverse asset classes to protect a portfolio so that a single market dip doesn't lead to financial ruin.

To move past this, one must adopt a "Work to Learn" mindset. Instead of choosing a job based on the salary, seek roles that teach you business systems, sales, and marketing. When you understand how money is "invented" through value creation, the fear of losing it diminishes.

3. "Broke" vs. "Poor": The Psychology of Wealth

Perhaps the most profound psychological distinction in wealth creation is the difference between being "broke" and being "poor."

"Broke is temporary, poor is eternal." — Rich Dad Poor Dad

This distinction highlights that wealth is not a number in a bank account; it is a mindset.

The Poor Mindset

Being "poor" is a state of mind characterized by a feeling of powerlessness. Someone with a poor mindset believes the government, their boss, or the economy is responsible for their financial state. They focus on Income Statements (how much they earn) and ignore their Asset Column.

Understanding Purchasing Power: A key missing link in education is the "Time Value of Money." A "Poor Mindset" views a savings account as the ultimate safety net. A "Wealthy Mindset" recognizes that if inflation is at 3% and your savings account pays 0.5%, you are actually losing 2.5% of your wealth every year. Wealthy individuals move money into "hard assets" (commodities, real estate, or business equity) that outpace the devaluation of currency.

The Wealthy Mindset (Even When Broke)

A person with a wealthy mindset may be "broke" (a temporary lack of cash), but they maintain a focus on their asset column. They understand that:

- Assets put money in your pocket (stocks, bonds, real estate, intellectual property).

- Liabilities take money out of your pocket (car loans, credit card debt, high-maintenance luxuries).

The psychology of long-term success requires the discipline to pay yourself first. By directing funds into assets before paying bills, you create a psychological "pressure" that forces you to think creatively and work smarter to cover your expenses.

Conclusion: Rewiring the Brain for Wealth

True financial freedom requires more than just a high salary; it requires a complete psychological overhaul of how we view work, risk, and education. If schools won't provide financial IQ training, the responsibility falls on the individual to seek out that knowledge.

By shifting from a mindset of "I can't afford it" to "How can I afford it?" you begin to see opportunities that others miss. Success is not about avoiding the fall; it's about having the financial education to turn every stumble into a step forward.

Explore more insights about “Rich Dad Poor Dad” by Elearnmarkets where we bridge the gap between traditional education and true financial freedom.