Are rising interest rates, tightening bank standards, and growing demand for long-term business stability forcing you to rethink how you finance commercial real estate in 2026? If so, you’re not alone. Across the United States, business owners, investors, and financial professionals are looking for smarter ways to secure stable, long-term capital and the SBA 504 loan for commercial real estate is increasingly the answer.

Commercial real estate financing has shifted dramatically in recent years, driven by macroeconomic forces, regulatory changes, and evolving lender behavior. In this environment, SBA commercial real estate loans, particularly the SBA 504 program, are emerging as a powerful tool for owner-occupied businesses seeking affordable, predictable financing.

This in-depth article explains how SBA 504 loans are reshaping commercial real estate financing in 2026, why they are gaining traction, and what that specifically means for businesses evaluating real estate acquisition, construction, or refinancing.

Understanding the SBA 504 Loan: A Foundation of Modern CRE Financing

The SBA 504 loan program is a government-backed commercial real estate financing tool administered by the U.S. Small Business Administration (SBA) and delivered through Certified Development Companies (CDCs). Its specific purpose is to help small businesses acquire major fixed assets such as land, buildings, and heavy equipment with long-term, fixed-rate financing.

Here’s how the financing structure typically works:

- 50% of the loan comes from a traditional lender (bank or credit union).

- 40% comes from a CDC backed by the SBA.

- 10% is the borrower’s down payment.

This unique structure makes SBA CDC 504 real estate financing highly attractive compared to conventional commercial loans that often require 20–30% or more upfront.

In 2026, the program continues to support business growth, job creation, and community investment while offering terms that many conventional lenders cannot match.

1. Lower Down Payments Preserve Business Cash Flow

One of the most transformative elements of the SBA 504 loan for commercial real estate is the low down payment requirement. While conventional commercial loans typically demand a 20–30% down payment or more, SBA 504 loans generally require only about 10% equity from the borrower.

This lower upfront cost is not just a convenience, it is a strategic advantage:

- More capital retained for operations: Businesses can preserve cash for payroll, inventory, or unexpected expenses.

- Reduced capital risk: Owners are less exposed if market conditions shift.

- Greater purchasing power: With less capital tied up upfront, some businesses can afford larger or higher-quality properties.

In an era where interest rate uncertainty persists and banks remain cautious, freeing up capital can make the difference between cautious leasing and confident ownership.

2. Long-Term Fixed Rates Reduce Financial Risk

In 2026, long-term fixed rate commercial loans are more valuable than ever.

The SBA 504 program offers fixed rates tied to long-term market indicators often tied to the 10-year U.S. Treasury note which helps protect borrowers from volatile rate movements.

According to recent rate trackers, SBA 504 rates for 25-year terms in 2025 hovered around 6.4%, a competitive level given current market contexts.

Compare that to many conventional commercial loans, where:

- Adjustable rates or balloon resets create refinancing risk.

- Interest rates may be higher or variable.

- Loan durations are often shorter, increasing monthly payment burdens.

For businesses that value predictability, these fixed rate structures are a major SBA 504 loan benefit for real estate. Knowing exactly what your monthly payment will be for 20–25 years simplifies budgeting and business planning.

3. Growing Demand for Owner-Occupied Commercial Properties

The commercial real estate landscape itself is shifting. Many business owners are rethinking leasing arrangements due to rising rental costs and market uncertainty. This trend is particularly evident in sectors like healthcare, manufacturing, logistics, and corporate headquarters, where owning real estate creates both equity value and operational stability.

This preference aligns directly with SBA 504 eligibility, the loan is designed for owner-occupied commercial real estate loans where:

- The business occupies at least 51% of the building (for existing properties).

- For new construction, occupancy requirements typically increase over time under SBA rules.

Owning rather than leasing not only builds equity but also shields businesses from future rental escalations and turnover disruptions. In 2026, many company owners are making this calculus more deliberately, especially as real estate markets adjust to post-pandemic demand patterns.

4. Construction Financing Is Becoming More Attainable

New construction projects used to be more difficult to finance due to higher risk and complex cost structures. In 2026, SBA 504 construction financing is helping business owners break ground more confidently.

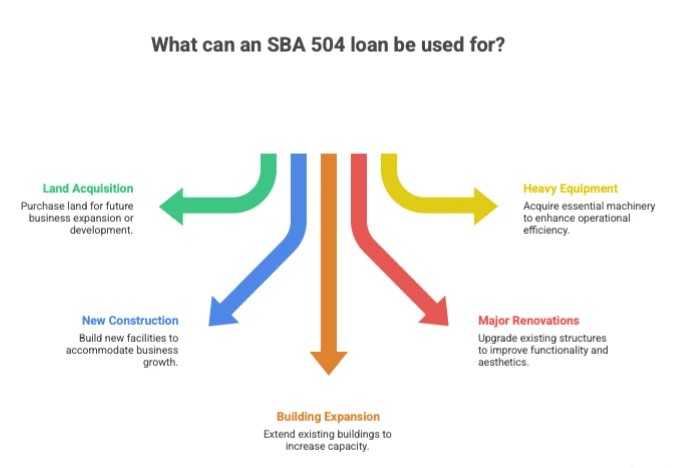

Through the program, eligible borrowers can use SBA 504 loans for:

- Land acquisition

- Ground-up construction

- Major building expansions

- Renovations and modernization

By delivering fixed, long-term capital and manageable down payments, SBA 504 financing enables businesses to:

- Build facilities tailored to operational needs

- Avoid costly lease expansions

- Accelerate growth without depleting working capital

This has become particularly important in industries where space customization matters — for example, medical facilities and industrial operations.

5. Refinancing Options Provide Stability and Growth Flexibility

Another lesser-known but powerful advantage of SBA 504 loans lies in refinancing.

Many businesses took out short-term or adjustable rate loans during previous periods of lower rates. As market rates rose and refinancing windows tightened, those businesses faced higher monthly costs and financial uncertainty.

With SBA 504 refinancing options, qualified borrowers can:

- Refinance existing commercial real estate debt into long-term fixed rates

- Extend amortization schedules for lower monthly payments

- Remove balloon payments that could disrupt cash flow

These features contribute valuable financial stability, especially for businesses planning expansion or capital improvements.

Statistical Trends That Support SBA 504 Engagement

While comprehensive SBA 504 data by loan count isn’t published in real-time, national reporting confirms key financing trends:

- The SBA supported $56 billion in small business financing in FY2024, a 7% increase year-over-year, indicating expanded capital access.

- For the first time since 2008, the SBA facilitated over 100,000 financing approvals across its programs, a 22% increase from 2023 and 50% higher than in 2020.

While this data includes all SBA loan types, it reflects a broader growth environment in which SBA-backed commercial real estate financing including SBA 504 loans, plays a significant role.

SBA 504 vs Conventional Commercial Loans: A Side-by-Side Comparison

Understanding the differences between SBA 504 and conventional commercial lending helps business owners make better decisions:

The SBA 504 loan often provides lower monthly payments, greater stability, and reduced refinancing risk — all reasons many business owners view it as preferable to traditional structures when evaluating long-term real estate investments.

Who Benefits Most From SBA 504 Loans in 2026?

SBA 504 financing is particularly compelling for:

- Businesses planning long-term occupancy

- Companies transitioning from leasing to owning

- Firms needing capital for construction or renovations

- Owners seeking better cash flow and financial predictability

If your business fits one of these scenarios, understanding SBA 504 loan benefits for real estate is not just academic, it can be strategically transformative.

Conclusion: Is an SBA 504 Loan Right for You?In 2026, commercial real estate financing is evolving driven by tighter bank standards, rising rates, and a greater emphasis on long-term viability. Against this backdrop, SBA 504 loans are emerging as a reliable, predictable, and owner-friendly financing option.

From lower down payments and long-term fixed rate commercial loans to flexible refinancing opportunities, SBA 504 financing addresses some of the biggest challenges facing business owners today.

If you are evaluating commercial property investment or want to learn more about whether an SBA commercial real estate loan (especially an SBA 504 loan for commercial real estate) fits your business plan, now is the time to act.

504 Capital Corporation specializes in SBA 504 lending, helping business owners throughout Virginia, North Carolina, and Maryland secure predictable, cost-effective financing for commercial property.

With deep expertise in SBA regulatory requirements, loan structuring, and strategic planning, 504 Capital Corporation guides borrowers through every step of the process. Their focus is not just on funding deals but on helping clients build sustainable businesses through thoughtful real estate investment.

Whether you’re buying, building, or refinancing in markets such as Virginia, North Carolina, and Maryland, 504 Capital Corporation can help you evaluate whether an SBA 504 loan aligns with your long-term goals.

Contact us to explore your options and get expert guidance tailored to your goals.