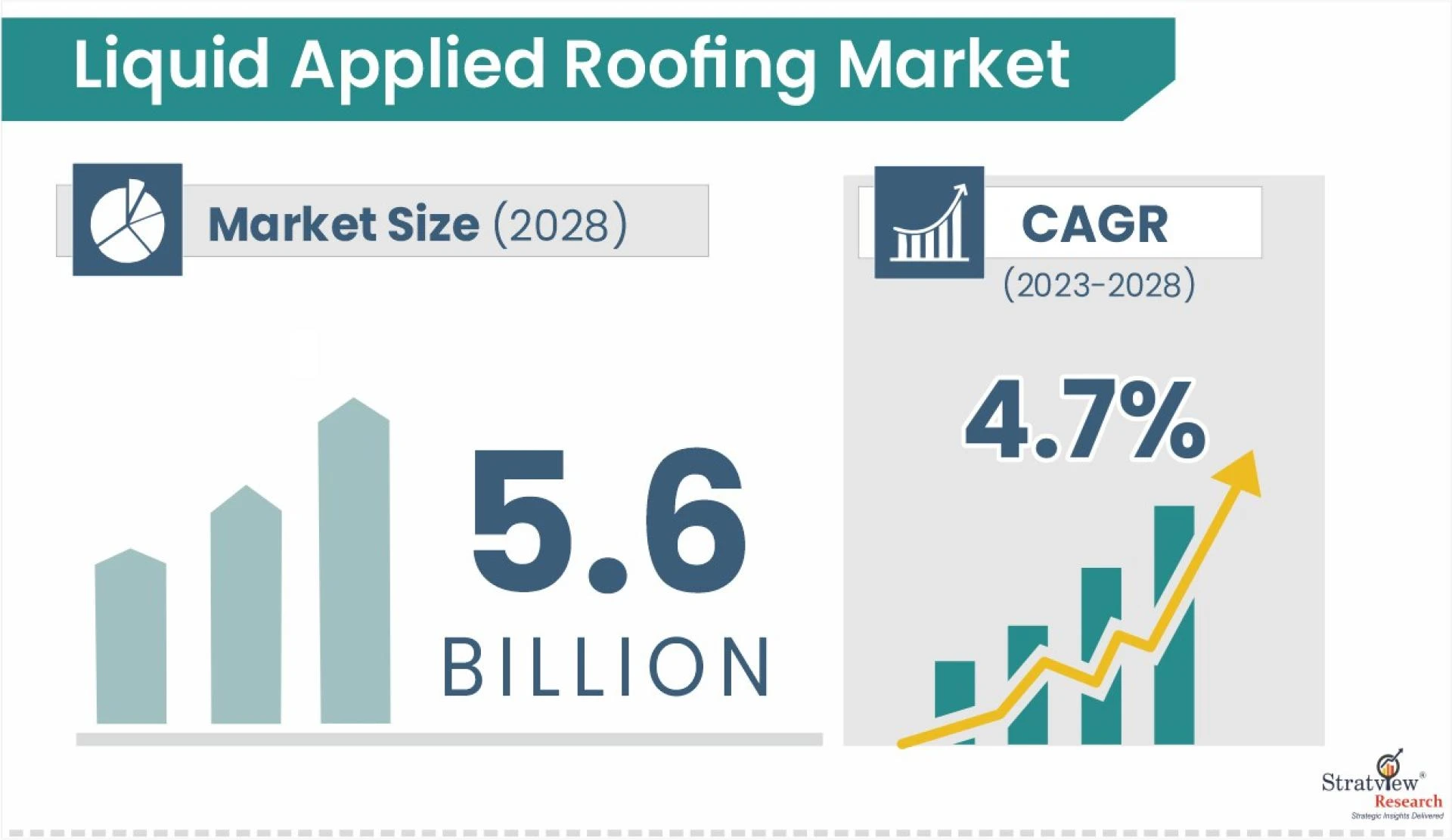

In North America, liquid-applied systems have evolved from niche to mainstream due to speed, reduced disruption, and the ability to extend roof life with reflective finishes. Stratview estimates the global liquid applied roofing market to grow at 4.7% CAGR (2023–2028), reaching USD 5.6 billion by 2028.

Download the Free Sample Report:

https://www.stratviewresearch.com/Request-Sample/789/liquid-applied-roofing-market.html#form

Drivers

- Lifecycle economics. LAR protects membranes against thermal cycling and UV, often avoiding tear-off and associated landfill costs—appealing to owners targeting lower total cost of ownership.

- Energy performance. Reflective coatings reduce cooling loads and improve comfort in hot weather, supporting energy-code compliance.

- Resilience & skills. Post-recession shifts and storm recovery highlighted fast, less-skilled deployment options; the methods have since become standard practice across many commercial portfolios.

Trends

- Materials: Acrylic is expected to remain the top material for its cost-effectiveness, durability, flexibility, and solar reflectance.

- Segments: Flat roofs and the commercial end-user segment dominate; repair & renovation outstrips new construction.

- Substrates: Concrete is the largest substrate, with bitumen also meaningful across residential and commercial installs.

- Country view: The USA remains the largest market, supported by housing starts, re-roofing cycles, energy codes, and the presence of major manufacturers (e.g., Carlisle, Garland, Sika USA, Johns Manville, GAF, Western Colloid, American WeatherStar, Polyglass USA).

- Corporate moves: Regional deal activity (e.g., IKO–Sika (2021) JV/asset moves; Gardner Gibson–ICP BSG (2021)) reflects continued portfolio tuning and channel expansion.

Conclusion

North American adoption is anchored in re-roofing ROI—fast overlays, fewer disruptions, and measurable energy benefits. Look for acrylic systems to lead, commercial flat roofs to concentrate volume, and U.S. demand to drive the region to USD 0.7B by 2028. Vendors combining proven chemistries with energy-efficient, code-aligned specs and strong contractor support will capture outsized share.