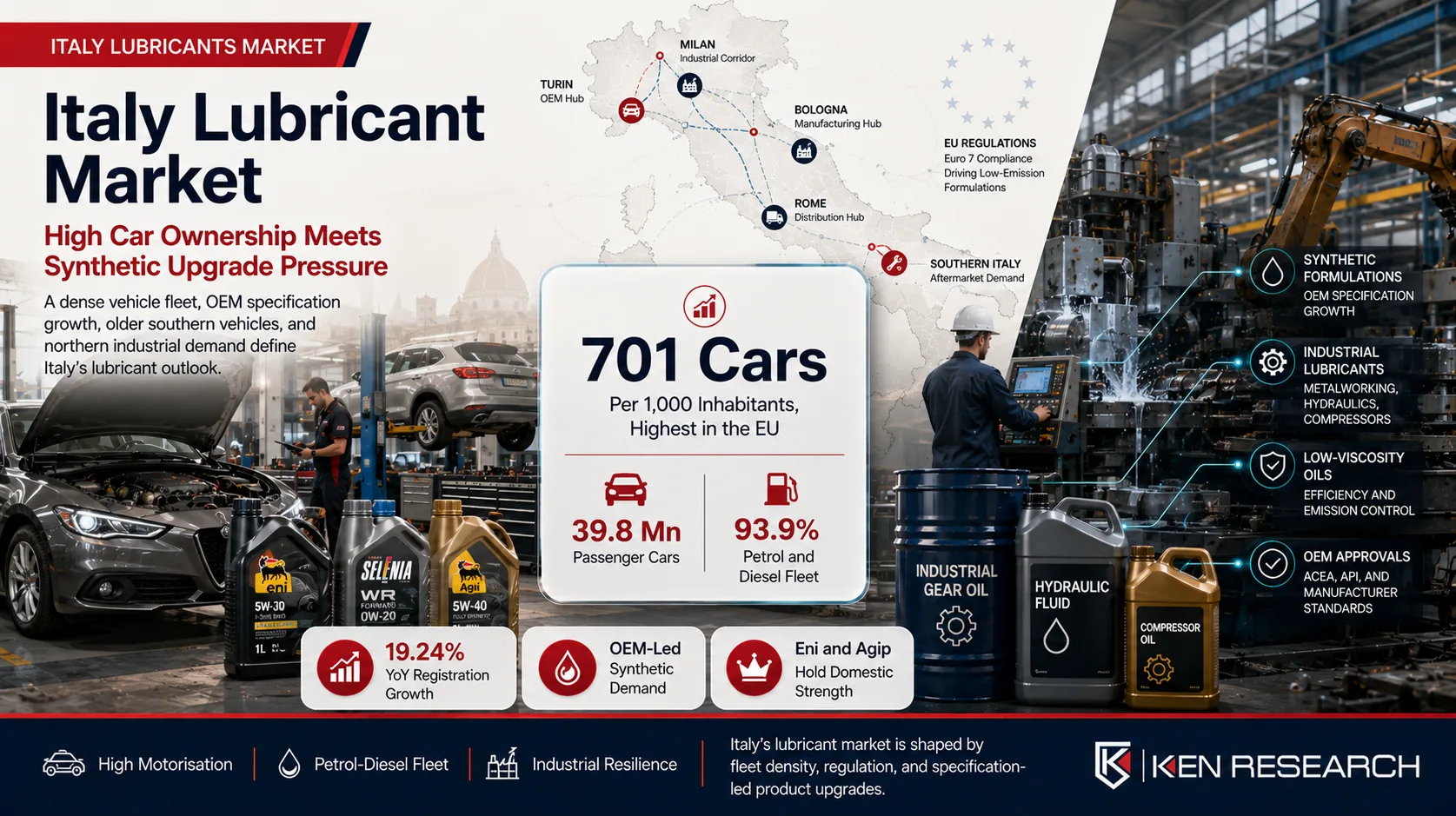

Italy holds the distinction of having the highest motorisation rate in the European Union, with 701 cars per 1,000 inhabitants in 2024, well above the EU27 average of 578, per Italy's National Statistics Institute (ISTAT). The total passenger car stock stands at approximately 39.8 million units, making Italy the fourth largest vehicle market in Europe by new registrations. Petrol and diesel vehicles still represent 93.9% of the total Italian vehicle fleet, sustaining strong demand for conventional and synthetic engine oils across a large and aging car parc. Italy sold over 1.79 million motor vehicles in 2023, a 19.24% year-on-year increase, reflecting fleet renewal momentum. Key players in the Italy Lubricant Market include Eni, Shell, ExxonMobil, Agip, TotalEnergies, and Castrol, competing across both automotive and industrial segments. The Italy Lubricant Market report by Ken Research covers market sizing, segmentation, competitive dynamics, and outlook to 2027.

Key Insights: Italy Lubricant Market

- Italy has the highest car ownership rate in the EU at 701 cars per 1,000 inhabitants, per ISTAT 2024

- Total passenger car stock approximately 39.8 million units, fourth largest vehicle market in Europe

- 93.9% of the Italian vehicle fleet runs on petrol or diesel, sustaining conventional lubricant demand

- New vehicle registrations grew 19.24% year-on-year in 2023, per OICA data, driving OEM-specified lubricant volumes

- South Italy has higher concentrations of older, more polluting vehicles, generating above-average per-vehicle lubricant consumption

- Automotive lubricants dominate total market share; industrial lubricants cover manufacturing, metalworking, and power generation

- Key players: Eni, Shell, ExxonMobil, Agip, TotalEnergies, Castrol, Fuchs

- EU REACH regulations and approaching Euro 7 standards are pushing the market toward low-viscosity synthetic formulations

What Shapes Demand in the Italy Lubricant Market

Italy's lubricant demand profile is driven by the intersection of a very large and aging vehicle fleet, a significant industrial base in the north, and a regulatory environment that is steadily pushing product specifications upward.

The motorisation rate of 701 cars per 1,000 inhabitants is the highest in the EU and significantly above markets like Spain (544) and France (579), per ISTAT. This vehicle density creates a structurally large addressable market for automotive lubricants. The aging dimension matters too: the south of Italy shows a notably higher concentration of older, more polluting vehicles, with a pollution index of 133.6 compared to roughly 110.7 nationally, per ISTAT. Older vehicles consume more lubricant per service interval, sustaining volume at the conventional grade tier while newer vehicles in northern urban centres pull demand toward low-viscosity synthetics.

Three dynamics shaping how the Italy Lubricant Market is evolving:

- OEM-led synthetic growth: Italy's vehicle manufacturing and assembly activity, combined with its role as a key European market for brands including Fiat, Alfa Romeo, Ferrari, and Maserati, means OEM-specified lubricants carry significant weight in determining product mix. New registrations growing 19.24% in 2023 have expanded the base of vehicles requiring factory-specification synthetic oils, lifting average product grade across the fleet.

- Industrial lubricant resilience: Italy's manufacturing sector, concentrated in the north around Milan, Turin, and the broader Po Valley industrial corridor, generates consistent demand for metalworking fluids, hydraulic oils, compressor oils, and industrial gear oils. The industrial segment is less exposed to EV-related volume risk than automotive and provides a stable demand base even through periods of automotive market softness.

- Euro 7 and REACH pressure: EU REACH regulations restrict harmful substances in lubricants and mandate environmentally acceptable formulations. Approaching Euro 7 vehicle standards will require even lower-viscosity, lower-SAPS engine oils across new vehicle platforms. Suppliers with strong synthetic R&D capability and established OEM relationships are best positioned to capture this specification-driven upgrade cycle.

Competitive Landscape of the Italy Lubricant Market

Eni holds a structurally advantaged position in the Italy Lubricant Market through its domestic brand recognition, refinery infrastructure, and the Agip lubricant brand's deep roots in Italian automotive culture. Shell and ExxonMobil compete across premium automotive and industrial segments. TotalEnergies has OEM partnership reach through its Stellantis relationships. Castrol (BP) focuses on premium automotive and two-wheeler segments. Fuchs targets industrial and specialty applications where performance specifications are highest. The competitive landscape in Italy is moderately consolidated at the top, with the major players competing primarily on product specification breadth, OEM approvals, and distribution network strength. For comparison of how a similar mature European market navigates the same regulatory and EV pressures, the UK Lubricant Market shows comparable competitive dynamics under a slightly different regulatory timeline.

Conclusion

Italy's lubricant market is defined by a paradox: the EU's highest car ownership rate generates the continent's most structurally large automotive lubricant demand base, yet the aging fleet and regulatory direction are simultaneously pushing product mix upward toward synthetics and lower-viscosity formulations. The industrial segment in northern Italy provides a durable second pillar of demand that insulates the market from pure automotive EV headwinds. Operators with OEM specification approvals, strong synthetic product lines, and reach into both northern industrial and southern automotive aftermarket segments will hold the most defensible positions as the Italy Lubricant Market evolves through 2027. The Italy Lubricant Market Outlook maps the competitive and regulatory trajectory in full.

FAQs

1. What makes Italy's vehicle fleet significant for the Italy Lubricant Market?

Italy has the highest motorisation rate in the EU at 701 cars per 1,000 inhabitants in 2024, per ISTAT, compared to the EU27 average of 578. The total passenger car stock is approximately 39.8 million units. With 93.9% of the fleet running on petrol or diesel, the addressable market for conventional and synthetic engine oils is among the largest in Europe. The combination of high vehicle density and an aging fleet, particularly in southern regions, creates durable and recurring lubricant demand well above European peers.

2. How does Italy's aging vehicle fleet affect the Italy Lubricant Market?

Southern Italy has a higher concentration of older vehicles, with a pollution index of 133.6 against a national average of 110.7, per ISTAT. Older vehicles consume more lubricant per service interval due to greater engine wear and seal degradation. This sustains demand for conventional mineral and semi-synthetic grades in the southern aftermarket, while northern Italy, with newer fleet composition and higher synthetic penetration, represents the premium tier of the market. The geographic split creates two distinct demand pockets requiring different product and distribution strategies.

3. Who are the key players in the Italy Lubricant Market?

Eni holds the strongest domestic position through its Agip brand and refinery infrastructure. Shell and ExxonMobil compete in premium automotive and industrial segments. TotalEnergies benefits from OEM partnerships with Stellantis brands. Castrol targets premium automotive and two-wheeler applications. Fuchs specialises in industrial and high-performance formulations. For detailed competitive benchmarking, the Italy Lubricants Market Analysis by Ken Research covers player-level market share and product portfolio positioning.

4. What is driving synthetic lubricant adoption in the Italy Lubricant Market?

Two forces are driving synthetic adoption in the Italy Lubricant Market. First, new vehicle registrations grew 19.24% year-on-year in 2023, expanding the base of vehicles with OEM-specified synthetic oil requirements. Second, EU REACH regulations and approaching Euro 7 standards mandate lower-viscosity, lower-SAPS formulations that push the entire market toward higher-specification products. OEM workshop networks are the primary channel pulling synthetic volumes through the market, while independent aftermarket channels follow as consumer awareness of longer drain intervals and engine protection benefits grows.

5. How is EV growth affecting the Italy Lubricant Market?

EV penetration in Italy is growing but remains at a minority share of total new registrations. Petrol and diesel vehicles still represent 93.9% of the Italian vehicle fleet as of 2024, per ISTAT, meaning conventional lubricant demand will remain structurally large for an extended period. EVs do reduce engine oil demand but generate new requirements for e-fluid and thermal management formulations. The near-term net effect on total lubricant volume is modest. The more immediate market force is regulatory: Euro 7 and REACH are reshaping product specifications faster than EV penetration is reshaping fleet composition.