When you need to sell and buy a home at the same time in Seattle, everything hinges on one question: what does your current home actually sell for?

You already know what you want next, but you can't make a strong offer while your current home is still unsold, and your savings alone rarely cover a second down payment. Most homeowners solve this with a contingent offer, tying the new purchase to selling the old one first. It feels like the safe choice, but in a market like Seattle's, where strong homes draw multiple offers, sellers can afford to pick buyers without conditions attached.

This guide walks through a process that lets you sell and buy at the same time, without a contingency, temporary housing, or carrying two mortgages at once.

The Home Sale Contingency Problem When You Sell and Buy a Home at the Same Time

A home sale contingency is a condition in your purchase offer. It says you'll buy the new home only if your current home sells first, usually by a set date. On paper, it protects you. You won't end up owning two homes at once, or scrambling to cover a down payment you don't have yet.

To a seller, that same condition looks different. They see a sale that depends on another sale they can't see, can't control, and can't speed up. Every seller wants a clean, predictable closing. A contingent offer adds a second unknown on top of the first one, and that unknown belongs to someone else.

The market you're in changes how much this matters when you sell and buy home at same time. In a buyer's market, homes sit longer, and sellers have fewer offers to pick from, so they may accept a contingency because the alternative is more waiting.

In a seller's market, like much of Seattle right now, homes often get several offers within days. A seller choosing between three clean offers and one contingent offer has an easy decision, and it's rarely the contingent one.

Some sellers who do accept a contingency add a kick-out clause. It lets them keep marketing the home while your contingency is active. If a stronger, non-contingent offer comes in, the seller can give you a short window to remove your contingency or walk away. The pressure that was supposed to protect you ends up right back on you.

The real fix isn't writing a better contingency. It's removing the need for one so you can sell and buy a home at the same time, starting with your home equity and a locked-in buyer for your current house.

How to Prepare Your Equity and Your Buyer Before You Sell and Buy a Home at the Same Time

Before you remove a contingency from your offer, you need one number: how much equity you have in your current home, the gap between its value and what you still owe. This number decides what options are open to you, so confirm it first, not last.

Most programs built for this purpose require a minimum equity position, generally around 22%. A real estate agent or lender confirms this by comparing your home's current market value to your remaining loan balance.

With equity confirmed, the next step is locking in a buyer for your current home. A listing is a hope; it waits for the right offer on its own schedule. A guaranteed purchase contract is different. It's a committed agreement on your current home, secured before you make an offer on a new one.

That guaranteed contract is what replaces the sell-first condition. Instead of telling a seller "I'll buy once mine sells," you can say your home is already under a binding agreement. No listing to wait on, no uncertainty about whether a buyer shows up.

This has to happen before you start shopping for your next home, not after. Equity confirmed, and a guaranteed buyer in place means every offer you make starts from strength, not hope.

Funding Your Down Payment When You Sell and Buy a Home at the Same Time

Confirming your equity and locking in a buyer solves two problems, but a third one shows up right behind them: your equity isn't cash yet. You still need funds for a down payment before your current home actually closes, and this is where most homeowners hit their next decision point.

Comparing the Common Ways Homeowners Fund the Gap

When that gap appears, most homeowners look at one of three familiar options to bridge it. Each one taps into the equity you already have, and each one can get you cash before your current home actually sells. The differences show up in the details: how the money is structured, what it costs you month to month, and how it affects your ability to qualify for the new mortgage you're trying to get approved for. Here's how the three most common choices compare.

Bridge loan

A bridge loan is a short-term loan against the equity in your current home. It gives you cash for a down payment, but it comes with interest and a monthly payment of its own. That new payment counts against your debt-to-income ratio right when your qualification for the new mortgage needs to look its cleanest.

HELOC (Home equity line of credit)

A HELOC is a credit line secured against your home equity, similar to a credit card with a variable interest rate. You can draw what you need, but like a bridge loan, it still adds a monthly obligation that shows up on your financial picture.

Cash-out refinance

A cash-out refinance replaces your current mortgage with a new, larger one and gives you the difference in cash. It resets your interest rate, which may not always work in your favor, and it adds new closing costs on top of the loan you already have.

A Lower-Cost Way to Fund Your Down Payment

There's a fourth option that works differently from the three above.

Instead of adding a new loan or resetting your mortgage, it lets you access an advance against the equity in your current home, before it sells, with no monthly payment while you own both properties at once.

That advance can go toward your down payment, closing costs, staging expenses, or moving costs, whatever strengthens your position for the new purchase. Because there's no monthly payment attached, it doesn't touch your debt-to-income ratio, so your qualification for the new mortgage stays exactly as clean as it would be without it.

Once your current home sells, the full amount is repaid automatically through escrow at closing. You never make a payment on it directly, and you're not carrying a second loan alongside your new mortgage while you wait for your old home to close.

How to Structure a Non-Contingent Offer and Sell and Buy a Home at the Same Time

By this point, three pieces are already in place: your equity is confirmed, a buyer is locked in for your current home, and your down payment is funded. That changes what your offer looks like on paper, and how a seller reads it.

Mortgage preapproval adds one more layer of strength. It tells the seller a lender has already reviewed your finances and confirmed what you can borrow. Paired with resolved equity and a funded down payment, it signals you're ready to close, not just interested.

With all three pieces resolved, your offer no longer needs a home sale contingency attached. There's no sell-first clause, no language tying your purchase to a second transaction. The seller sees a buyer who can close on schedule, nothing pending.

That's what lets a fully funded, non-contingent offer compete directly with cash buyers. Cash offers win by removing uncertainty, not just through money. An offer built this way removes that same uncertainty.

Given a choice between a slightly higher offer tied to another sale, and a clean offer they can count on, most sellers choose certainty. In a competitive market, that choice is often made before price ever enters the picture.

Closing, Selling, and Refinancing After You Sell and Buy a Home at the Same Time

With a non-contingent offer accepted, the hardest part of buying and selling a home at the same time is behind you. What's left is execution: closing on schedule, moving in without a gap, and turning the sale of your old home into a lasting financial advantage rather than just the end of the process.

Closing Quickly and Moving In Without a Gap

Once your offer is accepted, speed depends on how much is already resolved. Paperwork and underwriting can move fast, sometimes in under a week, because your equity, buyer, and financing were confirmed before you ever made the offer. By law, a primary residence still can't close in under two weeks, but that wait sits on the calendar, not on your file.

A fast, well-timed closing means you move directly into your new home. No storage unit, no short-term rental, no rent-back or leaseback arrangement to work out with a new buyer. Timing your close near the end of the month also helps you avoid overlapping mortgage payments on both homes at once.

Selling Your Former Home Vacant and Staged

Once you've moved out, your old home can go on the market the right way: empty, professionally staged, and without a deadline forcing you to take the first offer that comes in.

That distinction has a real dollar value. According to the National Association of Realtors' 2024 Profile of Home Staging, staged homes sell 33 to 50 percent faster and for 5 to 10 percent more than similar unstaged homes. On a Seattle home, a 5 percent premium is real equity that carries forward into your next move.

Turning Sale Proceeds Into a Lower Mortgage

Once your former home sells, the leftover equity doesn't have to sit idle. Applying it directly to your new mortgage balance lowers what you owe, and a lower balance can trigger a refinance that reduces both your rate and your monthly payment.

How the refinance structure keeps costs low

A typical refinance adds costs of its own: origination fees, appraisal, title, and settlement charges that can quietly add thousands back onto your balance. A refinance structure built for this purpose zeroes out or refunds those costs at closing, so you're not paying to save.

Why acting on small rate drops beats waiting

Because there's little to no cost each time, it makes sense to refinance as soon as rates move in your favor, even by a small amount, rather than waiting for a drop large enough to justify a traditional refinance's fees.

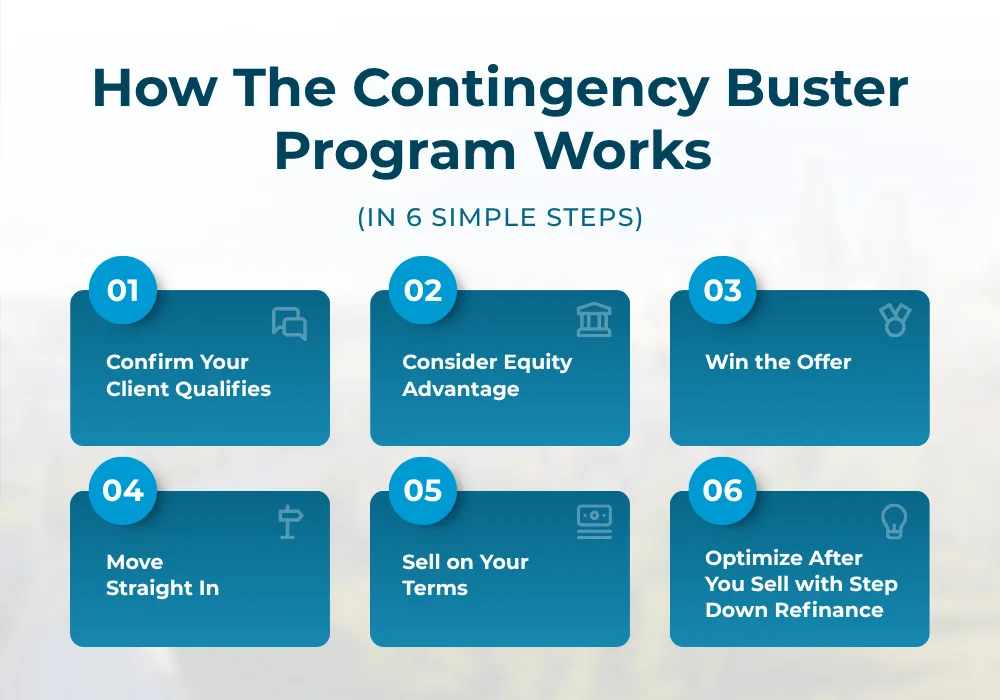

Buy the Home You Want With the Contingency Buster Program

Selling and buying a home at the same time in Seattle isn't complicated; it's usually just done in the wrong order. Confirm your equity first. Lock in a guaranteed buyer next. Fund your down payment without a bridge loan or a second mortgage. Then make an offer with nothing left for a seller to question.

That's exactly what the Contingency Buster Program from Seattle's Mortgage Broker is built to do. It removes the sell-first condition from your offer, keeps your budget intact through the move, puts your sale proceeds back to work, lowering your new mortgage, and makes it possible to sell and buy home at same time.

One conversation is all it takes to find out if you qualify. Reach out to Seattle's Mortgage Broker today and start your path to buying your next home without a contingency holding you back.

Frequently Asked Questions

Is It Better to Buy or Sell a House First?

Both come with trade-offs; buying first risks two mortgages, selling first risks temporary housing. The Contingency Buster Program removes that tradeoff by locking in a buyer for your current home before you make an offer on the next one.

Can You Close on a New House Before Selling Your Current One?

Yes. Once your down payment is funded and you have mortgage preapproval in place, you can close on your new home without waiting for your current one to sell first.

What Happens if Your House Doesn't Sell in Time?

With a guaranteed purchase contract already secured on your current home, this risk doesn't apply. Your buyer is locked in before you ever make an offer, so there's no waiting to see if a sale comes through.

What Is a Bridge Loan and How Does It Work?

A bridge loan is a short-term loan against the equity in your current home. It gives you cash for a down payment before your home sells, but it carries interest and a monthly payment of its own.

What Is a Home Sale Contingency, and Will Sellers Accept It?

A home sale contingency is a condition that ties your purchase to the sale of your current home first. Sellers often hesitate to accept one, especially in a competitive market, because it adds risk they can't control. One conversation with Seattle's Mortgage Broker can confirm whether you qualify to skip it entirely.