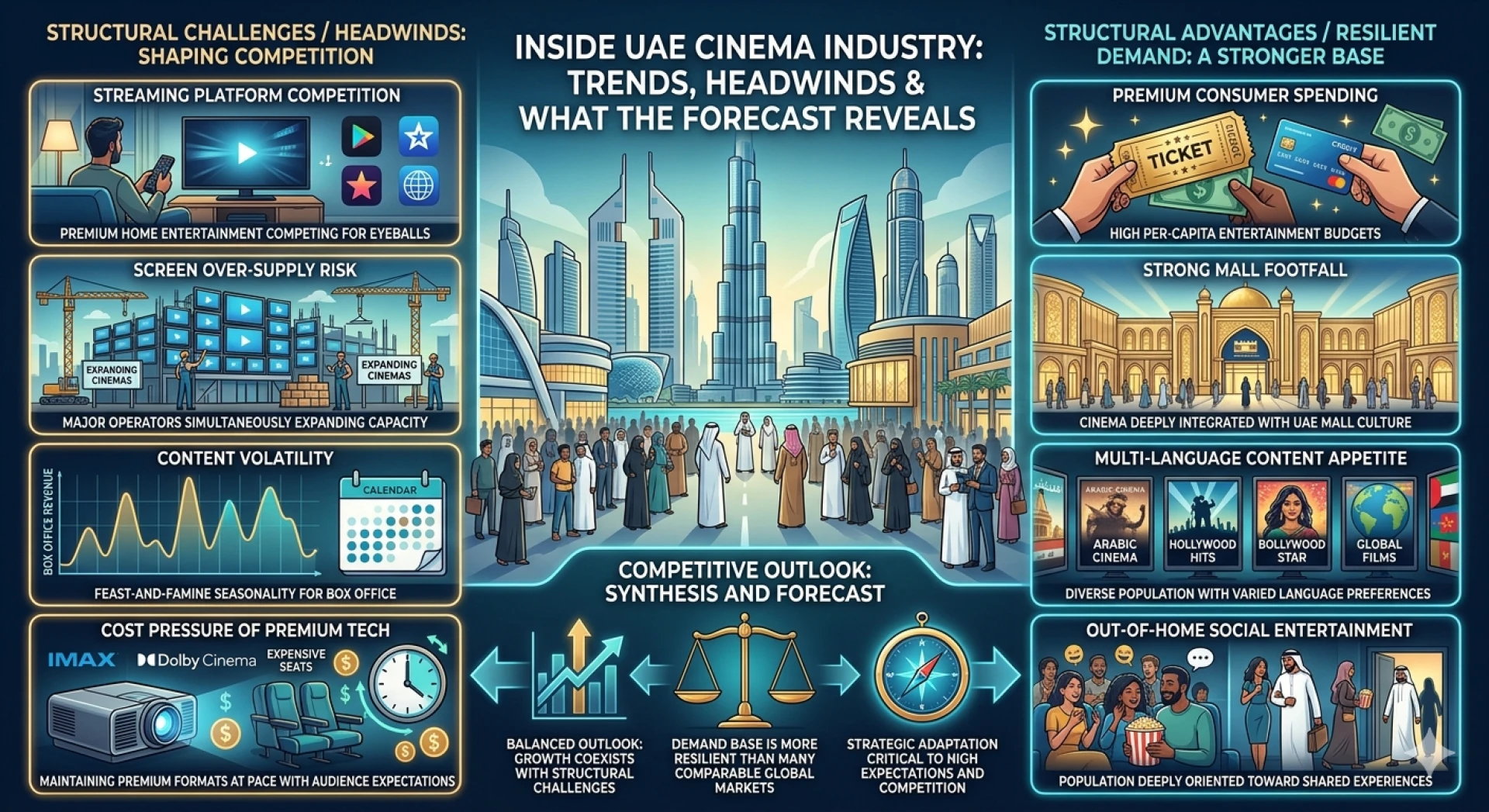

The UAE cinema competitive landscape is defined by a small group of well-capitalized operators competing on screen network scale, premium format portfolio, and mall footprint. How UAE cinema industry share is distributed reflects the commercial advantages of operators who secured anchor positions in the UAE's highest-footfall destination malls earliest, combined with the premium format investment levels that UAE consumers expect. VOX Cinemas dominates by screen count and format breadth across the UAE and wider Middle East. Novo Cinemas, Reel Cinemas, and MUVI Cinemas compete for the premium experience segment with differentiated format and location strategies. Empire Cinemas and HDR Cinemas represent smaller but regionally relevant competitive presences. The competitive dynamics among these players are increasingly driven by experience quality, loyalty program strength, and content access breadth rather than by geographic screen availability alone.

How UAE Cinema Competitive Structure Is Organized?

The UAE cinema competitive structure can be understood across two competitive tiers aligned by scale, format investment, and geographic coverage.

- Tier 1, National scale premium operators: VOX Cinemas with the widest UAE mall footprint and most extensive premium format portfolio; Novo Cinemas and Reel Cinemas with premium Dubai and Abu Dhabi mall positioning and well-developed VIP and luxury formats. These operators compete for the premium entertainment occasion spending that represents the highest revenue per visit in the market

- Tier 2, Segment and geography focused operators: MUVI Cinemas with a growing UAE presence and Saudi-market brand recognition; Empire Cinemas and HDR Cinemas serving specific geographic and audience segments with differentiated offerings. These operators compete on location specificity and audience segment relevance rather than national scale

- Luxury and boutique cinema concepts: Smaller operators developing ultra-premium private screening and boutique cinema concepts for corporate, social event, and ultra-premium individual audience segments who seek fully customized screening experiences beyond standard cinema formats

Competitive Structure Note: The UAE cinema market does not have a single dominant operator who serves all consumer segments without meaningful competition. VOX Cinemas leads by scale, but Novo and Reel Cinema are highly competitive in specific premium venue segments. MUVI is building its UAE presence with Saudi market brand recognition as a differentiator. This competitive environment benefits UAE cinema consumers through continued premium format investment and loyalty program development.

What UAE Cinema Industry Insights Reveal About Competitive Leaders?

The UAE cinema industry insights from competitive benchmarking identify premium format portfolio depth, mall anchor location quality, and F&B revenue development as the three dimensions that most reliably distinguish market leaders from secondary operators in the UAE.

- Premium format portfolio depth: IMAX, 4DX, Dolby Atmos, and VIP format availability across the majority of an operator's screen locations generating both ticket price premium revenue and the brand positioning that draws premium audience segments to their network ahead of competitors with narrower format portfolios

- Mall anchor location quality: Anchor screen positions in the UAE's highest-footfall destination malls, Dubai Mall, Mall of the Emirates, Yas Mall, Dubai Hills Mall, generating structural footfall advantages that cannot be replicated at secondary mall locations regardless of format investment

- F&B and ancillary revenue execution: Market leaders investing in full F&B menu quality, branded F&B partnerships, and in-seat dining capability that generates revenue per visit multiples above standard confectionery stand operations, creating a revenue model that is partially decoupled from box office fluctuations

Ken Research Report confirms that UAE cinema operators with the deepest premium format portfolio and highest-quality mall anchor positions generate the strongest revenue per screen in the market, with premium ticket pricing and F&B development creating compounding competitive advantages that secondary-location operators cannot replicate.

Where UAE Cinema Industry Competitive Dynamics Are Heading?

The UAE cinema industry report competitive trajectory points toward experience investment intensification as all major operators continue to upgrade format quality and F&B offerings in response to UAE consumer expectations and streaming competition pressure. Three competitive movements will define the next competitive phase.

- Geographic expansion into underdeveloped markets. All major operators have identified northern emirates and outer Dubai residential growth areas as geographic expansion priorities, with first-mover location advantage being the primary acquisition target for new screen development.

- Loyalty ecosystem investment. Major operators are investing in mobile app loyalty infrastructure that creates switching cost barriers through point accumulation, member-exclusive content events, and personalized promotion delivery that makes regular cinema attendance habitually tied to a single operator's loyalty program.

- Premium dining and event experience development. The transformation of cinema from a film viewing venue to a premium social dining and entertainment destination is the most consequential competitive trend. Operators who achieve this positioning generate audience retention that content calendar seasonality cannot easily disrupt.

The UAE cinema industry research report confirms that competitive share in the UAE cinema market will increasingly be determined by experience depth and loyalty program strength as geographic screen count differences narrow through simultaneous operator expansion across the UAE.

Ken Research Insights concludes that UAE cinema competitive leadership is being redefined from a screen count race to an experience quality and audience relationship depth contest, where premium format investment and loyalty ecosystem strength are the primary market share drivers.

Key Takeaway: UAE cinema industry share is concentrated among operators who combine premium format portfolio depth with high-quality mall anchor locations and F&B execution. Future share consolidation will be driven by loyalty program strength, experience quality investment, and geographic expansion into underdeveloped northern emirates markets.

Conclusion

The UAE cinema competitive landscape is evolving from a screen count competition to an experience depth and audience loyalty contest. VOX Cinemas, Novo Cinemas, Reel Cinemas, MUVI Cinemas, and their competitors are all investing in the experience dimensions, premium formats, in-cinema dining, loyalty programs, and geographic expansion, that will determine share distribution in the UAE cinema market through the decade ahead.

Frequently Asked Questions

Q1. How does VOX Cinemas maintain its UAE market leadership?

VOX Cinemas maintains UAE market leadership through the widest national screen footprint spanning Dubai, Abu Dhabi, Sharjah, and other emirates; the most extensive premium format portfolio including IMAX, 4DX, and VIP; strong digital infrastructure through the MyVOX loyalty app; and consistent content programming across Arabic, Bollywood, Korean, and Hollywood titles. Mall anchor positions in key destination centers provide structural footfall advantages that sustain utilization across the content calendar.

Q2. What distinguishes Reel Cinemas from other UAE operators?

Reel Cinemas benefits from its positioning as the cinema operator in Emaar mall properties including Dubai Mall, which is among the highest-footfall retail destinations in the world. This structural footfall advantage provides Reel with consistent audience access regardless of content calendar strength. Its premium Reel Gold VIP format and location quality within Dubai Mall give it a distinctive luxury positioning that differentiates it from competitors in the same Dubai market geography.

Q3. How are UAE cinema operators managing content access for different audience segments?

UAE cinema operators program multi-screen locations to simultaneously serve Bollywood, Arabic, Hollywood, and Korean content demand within the same cinema complex, optimizing auditorium sizing by language audience demand at each specific location. Premium and VIP auditoriums are typically allocated to the highest-demand English and Hindi titles, while mid-size screens serve Arabic and Korean content. Content programming requires sophisticated demand forecasting by location and audience demographic.

Q4. What technology investments are UAE cinema operators making in screen infrastructure?

Laser projector conversion from xenon lamp projection, Dolby Atmos and immersive audio system installation, motion platform 4DX seating installation, LED screen technology pilots, and high-brightness IMAX laser projection system upgrades are the primary technology investment categories across UAE cinema operators. These investments improve picture and sound quality, reduce energy consumption, and enable the premium format pricing and audience experience differentiation that drives revenue per visit growth.

Q5. How significant is private screening and corporate event revenue for UAE cinema operators?

Corporate and private event screening is a meaningful non-ticket revenue stream for UAE cinema operators, particularly in Dubai where corporate entertainment budgets and event culture generate demand for private screening buyouts, branded event activations, and launch event programming in cinema venues. Operators with the most premium screen environments and food service capabilities generate the highest private event revenue premiums and can sustain occupancy with corporate events during content calendar slow periods.