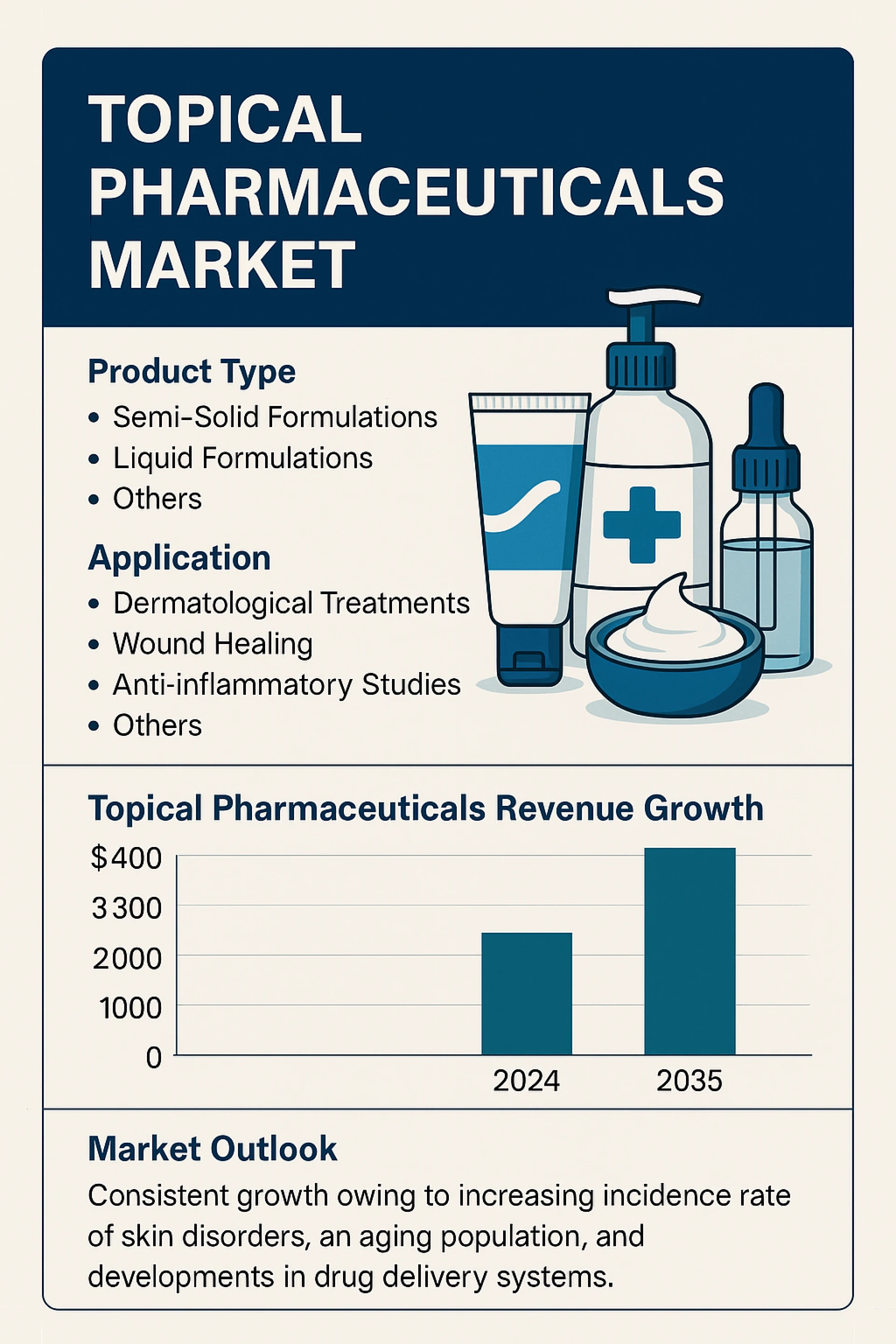

The global topical pharmaceuticals market has demonstrated remarkable resilience and growth, with its value reaching US$ 182.62 billion in 2024. Forecasts indicate that this sector is poised to more than double over the next decade, expanding at a robust 7.2 percent compound annual growth rate (CAGR) from 2025 through 2035 to achieve a valuation of US$ 396.30 billion by the end of the forecast period. Such sustained expansion underscores the vital role these localized therapies play in addressing a wide array of dermatological and mucosal conditions, as well as the industry’s capacity for innovation in drug delivery technologies and formulation science.

Analysts’ Viewpoint

Industry experts recognize several key factors driving the topical pharmaceuticals segment. First, the increasing incidence and prevalence of chronic and acute skin disorders—ranging from eczema and psoriasis to acne and fungal infections—have created escalating demand for therapies that can deliver active ingredients directly to affected sites with minimal systemic exposure. Second, demographic shifts, particularly the aging global population, have heightened demand for treatments that improve skin health, facilitate wound healing in elderly patients, and manage age‐related dermatological concerns.

Finally, advances in drug delivery platforms—such as liposomal carriers, microemulsions, and nanotechnology‐based systems—are enabling more effective penetration of active molecules through the skin barrier, improving both efficacy and patient adherence. Combined with strategic collaborations between pharmaceutical companies and biotech innovators, as well as a favorable regulatory environment for novel topical modalities, these trends have accelerated market growth and fueled robust R&D pipelines.

Market Introduction

Topical pharmaceuticals encompass a diverse array of dosage forms—including creams, ointments, gels, lotions, sprays, and patches—designed either for localized treatment of skin and mucosal conditions or for systemic delivery via transdermal patches. Their widespread adoption is largely due to the targeted nature of localized therapy, which limits systemic side effects and allows for higher local drug concentrations.

Chronic skin conditions such as atopic dermatitis, psoriasis, and acne often require long‐term management; topical routes therefore provide an essential means of therapy that patients can self‐administer, increasing convenience and compliance. The industry’s investment in formulation science has led to the development of combination products, enhanced permeation enhancers, and controlled‐release systems, further broadening the scope of indications that can be effectively treated via the skin.

Key Market Drivers

Rising Prevalence of Skin Disorders

Skin diseases represent one of the most common global health burdens, affecting nearly 900 million individuals worldwide. Dermatological conditions such as eczema, psoriasis, and fungal infections impose significant morbidity and quality‐of‐life challenges. For example, atopic dermatitis alone affects between 10 and 20 percent of children and 1 to 3 percent of adults globally.

Environmental factors—such as pollution, climate change, and increased allergen exposure—alongside lifestyle shifts, have contributed to rising incidence rates. Consequently, demand for topical corticosteroids, antifungals, retinoids, and emergent therapies such as topical Janus kinase (JAK) inhibitors is surging. The 2021 approval of Incyte’s Opzelura (ruxolitinib cream) for atopic dermatitis and vitiligo exemplifies the market’s appetite for first‐in‐class, targeted topical treatments.

Preference for Non-Invasive Drug Delivery

A major clinical and commercial trend in recent years has been the growing preference for non-invasive therapy. Topical formulations allow patients to bypass the gastrointestinal tract and first-pass metabolism, achieving local or systemic therapeutic effects without injections or pills. This is particularly important for pediatric and geriatric populations, where needle aversion and swallowing difficulties may impede adherence.

Common examples include diclofenac gel for osteoarthritis pain relief, which mitigates the gastrointestinal risks associated with oral NSAIDs. Advancements such as nanocarrier systems and liposomal gels continue to enhance drug permeation and retention in the skin, fostering patient acceptance and expanding the range of molecules amenable to topical delivery.

Semi-Solid Formulations Leading the Industry

Among product types, semi-solid formulations—comprising creams, ointments, gels, and pastes—account for the lion’s share of the topical pharmaceuticals market. Creams (oil-in-water emulsions) and gels (aqueous bases) offer ease of application and rapid absorption, catering to a broad spectrum of skin types. Ointments (water-in-oil emulsions), with their occlusive properties, are indispensable for treating dry, scaly lesions by promoting moisture retention.

Manufacturers are increasingly innovating within this segment through the incorporation of microspheres, liposomes, and combination APIs to enhance stability and targeted release. As consumer awareness of skincare grows, so does the demand for formulations that blend therapeutic efficacy with desirable cosmetic attributes—non-greasiness, minimal odor, and rapid drying time—further bolstering the semi-solid market’s prominence.

Regional Outlook

North America at the Forefront

In 2024, North America dominated the global topical pharmaceuticals market, propelled by high healthcare expenditure, advanced dermatological services, and proactive regulatory environments. The United States, in particular, benefits from strong R&D infrastructure and early adoption of novel drug delivery systems. An aging population prone to chronic skin conditions, coupled with high consumer awareness and a robust over-the-counter (OTC) market, supports robust demand across both prescription and non-prescription topical products. Canada similarly contributes through its growing biotech sector and public health initiatives that facilitate patient access to innovative therapies.

Growing Markets in Asia-Pacific and Beyond

Emerging markets in Asia-Pacific, Latin America, and the Middle East & Africa are witnessing accelerated growth rates, driven by rising disposable incomes, expanding healthcare access, and growing awareness of skin health and hygiene. Countries such as China, India, Brazil, and GCC nations are investing heavily in dermatological R&D, local manufacturing capabilities, and distribution networks, positioning them as attractive growth frontiers over the next decade.

Competitive Landscape and Key Players

The competitive environment within topical pharmaceuticals is characterized by a mix of global pharmaceutical giants and specialized dermatology firms. Major players include Bayer AG, Cipla, GSK plc, Johnson & Johnson, Novartis AG, Bausch Health, Merck KGaA, Galderma, Pfizer Inc., and Bristol Myers Squibb, among others. These companies employ strategies such as strategic partnerships, M&A activity, and lifecycle management to expand their topical portfolios and gain market share.

For instance, in April 2024, Cipla acquired Ivia Beauté’s distribution and marketing business to deepen its footprint in India’s personal care segment, while in February 2025, Glenmark Pharmaceuticals, in partnership with Cosmo Pharmaceuticals, secured UK MHRA approval for Winlevi, a first-in-class topical acne therapy.

Recent Developments

Cipla’s Strategic Acquisition (April 2024): Cipla Health Limited’s acquisition of Ivia Beauté Private Limited’s distribution and marketing business (Astaberry, Ikin, and Bhimsaini) underscores the company’s strategy to diversify into high-growth beauty and personal care segments.

Glenmark’s Winlevi Approval (February 2025): Glenmark Pharmaceuticals Ltd., collaborating with Cosmo Pharmaceuticals N.V., received MHRA approval for Winlevi (clascoterone cream), the first novel topical acne treatment in nearly four decades, offering a new mechanism of action for patients aged 12 and above.

The topical pharmaceuticals market stands at a dynamic crossroads of clinical necessity and technological innovation. With a strong foundation in semi-solid formulations and a burgeoning pipeline of advanced drug delivery systems, the sector is well-positioned to address a broadening spectrum of dermatological and systemic indications. As aging populations, rising prevalence of skin disorders, and patient preferences for non-invasive therapies continue to shape the landscape, companies that can deliver safe, effective, and cosmetically acceptable formulations will lead the way. Over the forecast period through 2035, the market’s projected growth to nearly US$ 400 billion highlights not only its commercial potential but also the critical role these therapies play in improving patient outcomes and quality of life worldwide.