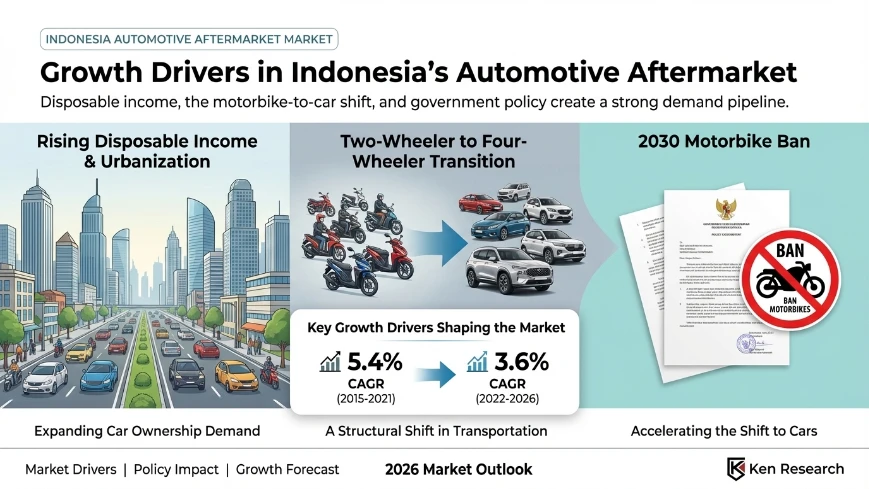

The Indonesia automotive aftermarket service market recorded a historical CAGR of 5.4% during 2015 to 2021, decelerating to a forecast CAGR of 3.6% through 2026, according to Ken Research.

Those two numbers tell a more specific story than they appear to. The slowdown is not a sign of a weakening market. It reflects a base that has already grown significantly, a parc dominated by older vehicles that generate steady rather than explosive service demand, and a competitive structure that is fragmenting rather than consolidating. The numbers are meaningful precisely because they are moderate and structural.

Understanding what sits behind this growth rate matters for OEM service centres, multi-brand operators, spare parts distributors, and investors mapping the Indonesian automotive services opportunity through the forecast period.

Indonesia Automotive Aftermarket Service Market Size: What the 5.4% Historical CAGR Built

The Indonesia automotive aftermarket service market size between 2015 and 2021 grew at 5.4% CAGR, per Ken Research. That rate compounded over six years produced a meaningfully larger revenue base than the starting point in 2015. The growth was driven by three concurrent forces: a rising vehicle parc as car sales grew across Indonesia, an ageing cohort of previously sold vehicles graduating into post-warranty, high-frequency servicing, and rising consumer awareness of the organized service sector.

The multi-brand workshop segment drove the majority of that revenue growth. Ken Research data shows that multi-brand service centres dominate the Indonesian aftermarket because post-warranty car owners, who make up the majority of the parc, consistently choose cheaper independent service over OEM authorized centres once manufacturer coverage expires. OEM centres captured the pre-warranty segment, which is smaller by volume and higher by average service price, while the larger post-warranty population flowed to multi-brand.

The vehicle type composition shaped which service categories grew fastest. MPV cars held the dominant share of the servicing market, driven by Toyota MPV demand across Indonesia. MPVs in commercial and family use accumulate mileage faster than passenger cars, generating above-average service frequency and repair and replacement revenue. Repair and replacement was the dominant service category across the review period, ahead of maintenance and body care, consistent with an older, higher-utilisation parc generating reactive rather than purely preventive service visits.

The spare parts market ran parallel to service growth. Ken Research notes that lubricants and oils led spare parts demand, followed by suspension and braking, electrical components, engine components, and consumables. The online spare parts channel began growing post-COVID, with Astra Otoparts and Pt. Daimaru Kogyo Indonesia named as major online marketplaces operating in this space.

Does 3.6% Mean the Indonesia Automotive Aftermarket Service Market Is Slowing Down?

A decline from 5.4% to 3.6% looks like deceleration, and arithmetically it is. But the Indonesia car service market growth context makes that reading incomplete. Ken Research's forecast through 2026 reflects a maturing market growing on a larger base, not a deteriorating one.

The structural demand driver is unchanged: cars aged 8 years and above contribute the majority to the car servicing market, per Ken Research, followed by the 3-8 years bracket and the 0-3 years group. As vehicles sold between 2015 and 2018 age into the 8-plus bracket, they add to the dominant service volume cohort continuously. That is not a decelerating demand dynamic. It is a steady, parc-fed demand engine.

What moderates the rate is the competitive environment. Ken Research identifies the influx of new players and car variants from abroad as a named growth contributor, but also a source of competitive fragmentation. More brands means more service complexity, more spare parts variety, and more pressure on any individual operator's share. The market grows in aggregate while individual operator revenue grows more slowly.

The forecast through 2026 also anticipates organized multi-brand expansion into Tier I cities, per Ken Research. That geographic push will intensify competition with OEM authorized workshops including Auto 2000, Honda Indonesia Mobil, and PT Nissan Motor Indonesia in urban markets. Competition rising while demand stays steady produces a lower growth rate for incumbents even as total market revenue increases.

For regional context, the Vietnam automotive aftermarket service market shows a comparable CAGR moderation at a similar stage of market development, where parc-driven steady demand rather than adoption-phase growth sets the rate. The Vietnam automotive aftermarket service market provides that Southeast Asian benchmark on CAGR trajectory as aftermarket markets mature.

What Does the Indonesia Automotive Aftermarket Service Market Forecast Actually Signal for Operators?

The Indonesia automotive aftermarket service market outlook to 2026, per Ken Research, signals three practical implications for operators and investors.

- Multi-brand expansion is the volume play Ken Research anticipates organized multi-brand operators moving into Tier I cities through 2026, going head-to-head with OEM centres in Jakarta and other high-density markets. Operators with standardized service models and multi-brand capability are better positioned than those dependent on a single brand franchise or a single city presence.

- Online booking and spare parts are the efficiency plays The majority of car service bookings remain offline, per Ken Research, with OEM companies having introduced online booking while most multi-brand centres lag. The online spare parts channel is growing post-COVID. Both represent low-penetration channels with demonstrable upward momentum through 2026.

- The western region anchors near-term revenue Jakarta and the surrounding western region dominate car service demand, per Ken Research, due to population concentration and the highest number of car sales. Central and eastern Indonesia follow but lag on organized service penetration. Geographic expansion east is a medium-term play, not a 2026 priority for most operators.

The 3.6% CAGR is not a ceiling. It is a baseline that a well-positioned operator can exceed through geographic expansion, service mix optimization, and online channel investment, all of which Ken Research identifies as active development vectors in the market through 2026.

Conclusion

The Indonesia automotive aftermarket service market's 5.4% historical CAGR from 2015 to 2021 built a solid revenue base anchored by post-warranty vehicle demand, multi-brand workshop dominance, and repair and replacement as the leading service category, as documented by Ken Research. The 3.6% forecast CAGR through 2026 reflects steady parc-driven growth rather than deceleration, with cars aged 8 years and above continuing to generate the highest service volume. Multi-brand operators including Bosch Auto Care Service, CARfix, and Autoglaze Indonesia are positioned to expand into Tier I cities as Ken Research forecasts, intensifying competition with OEM centres. Toyota remains the dominant brand in both car sales and service demand, with Japanese brands setting the tone for spare parts supply chains and technician skill requirements across the full market.

This blog is based on insights from the Indonesia automotive aftermarket service market report published by Ken Research, covering sizing, segmentation, competition, drivers, challenges, and outlook. If you want deeper analysis on this market, you can check it out.

FAQs

1. What is the forecast CAGR for the Indonesia automotive aftermarket service industry through 2026?

According to Ken Research, the Indonesia automotive aftermarket service market is forecast to grow at a CAGR of 3.6% from 2021 to 2026, decelerating from the 5.4% recorded during 2015 to 2021. The moderation reflects a maturing market growing on a larger base, not a demand decline.

2. Why did the car service CAGR in Indonesia decline from 5.4% to 3.6%?

The decline from 5.4% to 3.6% reflects competitive fragmentation from new players entering the market, a larger revenue base over which growth is measured, and steady parc-fed demand rather than an adoption-phase surge. Ken Research notes that the influx of new car variants and players is a named growth contributor that also intensifies competitive pressure on individual operators.

3. Which workshop segment accounts for the majority of revenue in Indonesia's car service industry?

Multi-brand workshops account for the majority of revenue in the Indonesian car servicing industry, per Ken Research. Post-warranty car owners, who make up the bulk of the vehicle parc, consistently prefer the lower service fees of multi-brand operators over OEM authorized centres once manufacturer coverage expires.

4. How does the vehicle parc composition affect aftermarket service demand in Indonesia?

Ken Research data shows that cars aged 8 years and above generate the highest service volume in the Indonesian aftermarket, followed by the 3-8 years bracket. The majority of cars in the Indonesian parc are above four years old, meaning most service demand is structurally concentrated in age cohorts that require more frequent and more extensive work than newer vehicles.

5. What are the key opportunities in the Indonesian car aftermarket through 2026?

Ken Research identifies organized multi-brand expansion into Tier I cities, growth in online spare parts purchasing through platforms like Astra Otoparts, and increasing adoption of online service booking as the key opportunity vectors in the Indonesian automotive aftermarket through 2026. The western region anchored by Jakarta remains the highest-revenue geography in the near term.