Something significant is straining the backbone of the American energy system — and it has nothing to do with a lack of generation. Wind farms, solar installations, and natural gas plants are coming online. The problem is getting their output to the people who need it. Transmission infrastructure, much of it designed decades ago for a very different economy, is struggling to keep pace with a demand environment it was never built to handle.

The head of the North American Electric Reliability Corporation didn't mince words at a recent industry gathering, describing the current situation as a "five-alarm fire" for grid reliability. The language was stark — and intentional. This is an agency known for measured, technical communication, not alarm-raising. When their leadership starts using emergency metaphors, it's worth paying attention.

So what, specifically, is putting so much pressure on the grid? And why is a technology that involves simply swapping out old wire — reconductoring — gaining serious traction as one of the most viable solutions available right now?

A Demand Surge Unlike Anything the Grid Was Designed For

U.S. electricity consumption isn't climbing gradually — it's accelerating. The Energy Information Administration projects that national power demand will hit all-time highs in both 2025 and 2026. This isn't a seasonal blip or a post-pandemic rebound. It reflects a fundamental rewiring of the economy: electrified transportation, onshore manufacturing, and — most significantly — the explosive growth of digital infrastructure.

Data centers are now the single largest driver of new load on the grid. Utilities across the country have flagged 166 GW of anticipated peak demand growth, and roughly 90 GW of that is attributable to data centers alone. What makes this load particularly difficult to manage is its profile: AI computing clusters operate continuously at high capacity, 24 hours a day, producing a relentless baseline draw that never really lets up.

The problem is also intensely geographic. In Virginia — home to one of the world's largest concentrations of data infrastructure — data centers are responsible for more than 90% of all new projected electricity demand. The grid there wasn't built for that kind of concentrated load. Across PJM's market territory, which covers states from Illinois to the Carolinas, the surge in data center development drove a $9.3 billion spike in the 2025–26 capacity auction. Households in Ohio and western Maryland are expected to see monthly bills climb by roughly $16 to $18 as a direct consequence.

Those rate increases will land on people who had no role in the data center build-out. They're simply living in the same region.

The Case for New Lines — And Why It Falls Apart in Practice

When a transmission network runs short on capacity, the textbook response is to expand it. Build new lines. Carve new corridors through the landscape. Connect more substations. In theory, this is straightforward infrastructure investment.

In practice, it's an extraordinarily slow process. The DOE's own 2024 National Transmission Planning Study estimates the country needs to add roughly 5,000 miles of high-capacity transmission every year to keep pace with demand. The actual figure completed in 2024? Just 322 miles — the third-lowest annual total in a decade and a half. Back in 2013, the industry managed to complete nearly 4,000 miles in a single year.

The gap between what's needed and what's being built isn't closing — it's widening.

Building new transmission corridors requires assembling land rights across potentially hundreds of property owners, clearing environmental review processes that frequently take years, navigating state and federal regulatory approval chains, and overcoming organized local opposition. Projects that clear all of those hurdles can still spend a decade in pre-construction. For companies that need reliable power delivery within the next two or three years, that timeline is simply incompatible with their planning horizons.

Reconductoring: The Upgrade That Works Within What Already Exists

Reconductoring is, at its core, a swap. You pull out the aging wire running along an existing transmission tower and replace it with a far more capable advanced conductor — without touching the towers, the land, or the permits that govern that corridor.

Why does this matter so much? Because the real bottleneck in most transmission lines isn't the towers or the route. It's the wire itself. Traditional conductors heat up as power flows through them, and as they heat up, they sag. That sag reduces clearance from trees and ground, so grid operators have to cap how much power flows through the line — not because the towers can't handle more, but because the wire would droop too close to something it shouldn't.

Advanced conductors — particularly high-temperature, low-sag designs and composite-core conductors — are engineered to carry much higher currents while sagging far less. The same towers. The same right-of-way. Dramatically more capacity.

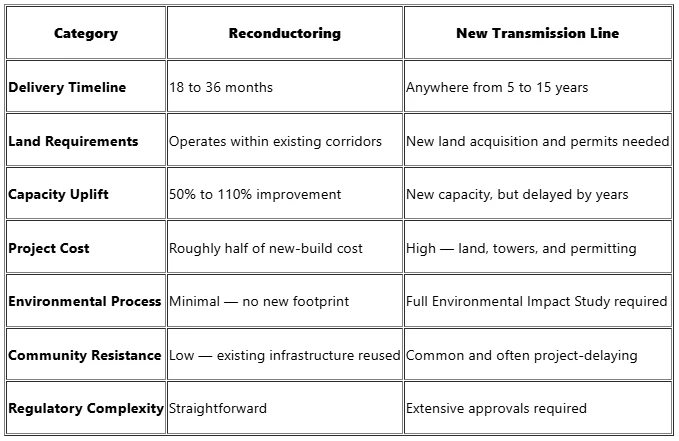

What Reconductoring Delivers — At a Glance

✓ Project completion in 18 to 36 months, compared to 5 to 15 years for new lines

✓ Capacity gains of 50% to 110% over the original line rating

✓ Cost roughly half that of constructing equivalent new transmission

✓ No new land, no new towers, no new permits required

What the Research Actually Shows

The most rigorous independent analysis of reconductoring's potential comes from UC Berkeley's Goldman School of Public Policy, conducted in partnership with GridLab. The scale of the opportunity they documented was larger than most industry observers expected.

Swapping out conventional conductors across the existing transmission network could generate approximately 64 TW-miles of additional interzonal transfer capacity by 2035 — roughly four times more than a strategy focused exclusively on building new lines, which would yield only about 16 TW-miles over the same period. The cost premium for achieving that much greater capacity uplift is modest: around 20% more than a new-build-only approach.

The clean energy implications are equally striking. That additional transmission capacity would give the U.S. a viable path to sourcing 90% of its electricity from zero-carbon generation by 2035 — not because reconductoring is a climate technology per se, but because more transmission capacity means more ability to move renewable energy from where it's generated to where it's consumed.

Pair reconductoring with meaningful reforms to the greenfield permitting process, and the combined economic benefit is estimated at over $400 billion in avoided system costs relative to business as usual. That's not a marginal efficiency gain. It's a figure that changes the math on the entire energy transition.

The Regional Stress Points

Transmission congestion isn't a uniform national problem — it concentrates in specific markets where load growth has outrun infrastructure investment most dramatically:

- ERCOT (Texas) is contending with projected load additions of 53 GW through 2030 — equivalent to a 62% jump above its existing peak demand record.

- PJM faces 30 GW of additional growth, the bulk of it tied to data center expansion across Virginia and surrounding states.

- SPP and MISO each absorbed $1.8 billion in congestion costs during 2024, as existing lines hit their limits and power couldn't move freely across the network.

- Nationally, total U.S. transmission congestion costs topped $12 billion in 2024 — and that figure likely understates the true cost, as interregional constraints are notoriously difficult to fully quantify.

Congestion costs aren't abstract financial metrics. They represent electricity that couldn't reach the customers who needed it efficiently — and the difference gets passed along in the form of higher rates and lower system reliability.

Policy and Capital Are Catching Up

For years, reconductoring was treated as a routine maintenance practice rather than a strategic capacity tool. That framing is shifting as policymakers and investors recognize the speed advantage it offers relative to greenfield alternatives.

The Department of Energy committed a $1.6 billion loan guarantee to support the reconductoring of approximately 5,000 miles of transmission infrastructure across five states — one of the largest single federal investments in a grid upgrade technology to date. The projected outcome is a capacity increase of around 70% across the affected corridors.

At the state level, California's grid operator CAISO approved five reconductoring projects in its 2024–2025 transmission plan, all using advanced conductor technology — incorporated into a broader $4.8 billion grid modernization program that avoids the need for new corridor development.

Research from RMI suggests that upgrading existing infrastructure — rather than building new — could accommodate as much as 95% of the anticipated load growth now appearing on utility forecasts. That finding reframes the entire debate. The question isn't whether the grid needs investment. It's whether that investment has to take the form of brand-new construction.

Where Reconductoring Reaches Its Limits

None of this is to suggest that swapping wires solves every grid problem. It doesn't, and utility planners need to be clear-eyed about where the approach runs out of road.

Reconductoring works best on shorter lines. For the relatively small share of the network — roughly 2% — where spans exceed 50 miles, the dominant constraints shift from thermal sag to voltage stability and angular stability issues that conductor upgrades alone can't address. Those situations often require additional substation equipment, reactive power support, or new infrastructure along the route.

There are also genuinely new corridors that the grid needs — routes that don't exist in any form today, connecting regions that currently have no transmission link between them. No amount of reconductoring can substitute for a line that hasn't been built yet. In those cases, greenfield development remains the only answer.

GridLab's analysis anticipates that demand for new corridor construction will grow through the 2030s as the most viable reconductoring opportunities are progressively utilized. The two approaches aren't alternatives — they're stages. Reconductoring addresses what can be fixed fast; new construction addresses what can only be built over time. Getting both moving in parallel is the actual goal.

The Practical Takeaway

The U.S. transmission network wasn't engineered for the world it now has to serve. It predates the data center era, the electrification of transportation, and the large-scale integration of variable renewable generation. The distance between what the grid can currently handle and what the economy is about to ask of it is measurable and growing.

Closing that distance requires multiple tools working simultaneously. New transmission will eventually be necessary. But new transmission takes time that many regions don't have. Reconductoring doesn't require new land, new permits, or new community negotiations. It uses the infrastructure society has already invested in — and substantially increases what that infrastructure can deliver.

The grid crisis is real. The urgency is real. But so is the solution — and a significant part of it is already strung between towers, waiting to be replaced with wire that can do far more.