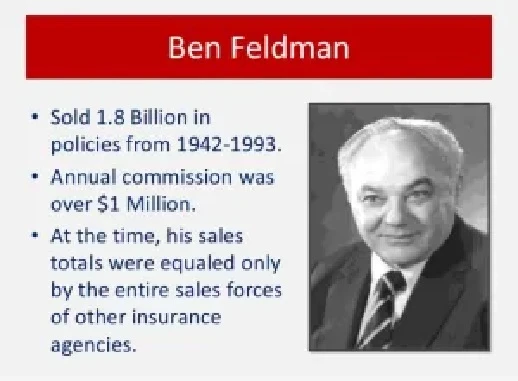

Great salespeople don’t chase policies. They chase purpose. That mindset changed the insurance industry forever. Within the first few moments of studying Ben Feldman's life insurance sales, you realize he never focused on pushing products. Instead, he refined life insurance sales techniques that centered on service, urgency, and disciplined execution—especially for families who needed guidance the most.

As technical college instructors and CTE program directors, you prepare students for real-world careers. When you examine Ben Feldman's life insurance sales, you uncover a blueprint that transforms average producers into trusted advisors. His philosophy doesn’t rely on gimmicks. It relies on clarity, courage, and consultative selling frameworks that align perfectly with how modern professionals should serve middle-income markets.

Sell Value, Not Policies

You already teach students that technical skill alone doesn’t create career success. The same principle applies here. Feldman didn’t “sell life insurance.” He sold what life insurance does. He sold certainty. He sold protection. He sold opportunity.

When you apply that shift in thinking, everything changes. Instead of leading with features—cash value, term length, riders—you lead with outcomes. You ask: What happens to your family if income disappears? What happens to college plans? Retirement?

That pivot from product-first to outcome-first forms the backbone of modern consultative frameworks. Today’s strongest life insurance sales techniques mirror that approach. They guide clients to see gaps. Then they move decisively to close them.

Sell During Hard Times—Build Skill for Any Time

Economic pressure separates average agents from professionals. Feldman insisted that you must learn to sell during downturns so you can thrive in strong markets. That principle still holds.

Middle-income families often hesitate because headlines scare them. They worry about affordability. They assume they must wait. Instead of retreating, you lean in. You sharpen your conversations. You refine your messaging. You show clients how protection stabilizes uncertainty.

When you teach future advisors this resilience mindset, you prepare them for sustainable careers—not seasonal success.

Harness the Buyer’s Best Interest

Here’s where Feldman truly reshaped the field. He recognized that families don’t wake up wanting insurance. They wake up wanting relief. Relief from debt. Relief from stress. Relief from financial confusion.

So you stop pitching. You start diagnosing.

You ask better questions. You dig into cash flow. You examine spending leaks. You uncover unused resources. That strategy aligns directly with the “find the money” philosophy widely used today in middle-income markets.

Modern consultative systems—especially those designed for underserved families—teach agents to uncover hidden dollars within existing budgets. Instead of competing for wealthy clients, you help everyday earners restructure finances. You show them how to redirect money toward protection and future wealth-building.

That approach carries the DNA of Ben Feldman's life insurance sales philosophy. It respects the client’s reality while elevating their possibilities.

The Power of the Disturbing Question

Feldman famously emphasized the interview. Not a casual chat. Not a rushed quote. A structured, intentional fact-finding session.

He understood something critical: awareness drives action.

When you ask surface-level questions, you get surface-level commitment. But when you ask what he called a “disturbing question,” you create clarity. What happens if income stops tomorrow? What happens if retirement savings fall short?

You don’t manipulate. You illuminate.

In CTE education, you already use this method. You challenge students to think critically about consequences. Feldman applied the same logic in sales. Today’s most effective life insurance sales techniques build around this disciplined discovery process. They turn interviews into transformation moments.

Client-Specific Solutions Drive Momentum

Generic illustrations don’t inspire urgency. Personalized strategies do.

Once you uncover financial inefficiencies, you show clients exactly where money hides. You outline how they can protect their family and still save for college or retirement. You connect coverage to real goals—not abstract benefits.

Programs that train agents to serve middle-income markets emphasize structured marketing, appointment-setting frameworks, weekly coaching, and disciplined follow-up. They don’t encourage aggressive selling. They encourage strategic advising.

That structure matters. New agents often fail because they lack repeatable systems. Feldman thrived because he committed to consistent habits. Modern platforms that provide scripts, training libraries, and live coaching simply operationalize what he practiced decades ago.

Middle-Income Markets: The Untapped Opportunity

Many agents chase affluent prospects because they assume higher premiums equal easier income. Feldman proved otherwise.

Middle-income families represent scale. They represent loyalty. They represent referrals. When you serve them well, you build sustainable momentum.

Instead of fighting over a small wealthy segment, you educate broad communities. You host workshops. You build joint ventures. You maintain consistent communication. You stay visible.

You don’t act like a salesperson. You act like a financial guide.

For instructors shaping the next generation of advisors, this shift matters deeply. Students entering financial services must learn how to build trust-based practices, not transactional pipelines. When you embed these principles into your curriculum, you align classroom learning with real-world success.

Sell Yourself First

Feldman often said your most important sale involves selling yourself. Confidence, preparation, and conviction create influence.

If you doubt your value, clients sense it instantly. But when you commit to disciplined study, ongoing coaching, and structured practice, you project certainty.

Modern training ecosystems—particularly affordable membership-based platforms that offer weekly live sessions, case design classes, and marketing systems—reflect this belief. They reinforce skill development and accountability. They equip agents to become trusted advisors rather than product pushers.

That transformation sits at the heart of sustainable middle-income outreach.

Conclusion: A Philosophy That Still Leads the Industry

The genius behind Ben Feldman's life insurance sales philosophy lies in its simplicity. Sell during hard times. Ask better questions. Sell value, not products. Provide personalized solutions. Focus on families who truly need guidance.

When you integrate those lessons into modern consultative frameworks, you elevate today’s life insurance sales techniques beyond transactional selling. You teach future advisors how to help middle-income families find the money, protect their income, and build security without chasing wealthier demographics.

For technical educators and program directors, this philosophy offers more than historical insight. It offers a replicable model for career readiness. When you train students to think like disciplined problem-solvers—grounded in the mindset behind Ben Feldman's life insurance sales and refined through proven life insurance sales techniques—you don’t just prepare them to sell. You prepare them to lead, serve, and build lasting impact in communities that need them most.