Stationary fuel cells have crossed a critical threshold in Asia-Pacific: they are no longer an emerging technology demonstrating proof of concept but a deployed infrastructure asset that Japan and South Korea are integrating into national energy policy at scale. The APAC Stationary Fuel Cell Market is valued at USD 1.30 billion in 2023, driven by rising demand for clean, efficient energy solutions across residential, commercial, and industrial sectors. Japan's Basic Hydrogen Strategy, launched in 2020 and ongoing through 2024, targets expanded hydrogen utilization in fuel cells with a projected investment of USD 1.5 billion annually. South Korea's Hydrogen Economy Roadmap supports hydrogen adoption across energy systems through hydrogen clusters and refueling infrastructure. These are not exploratory programs. They are funded, multi-year deployment commitments that are building the structural foundation for stationary fuel cell expansion across the region.

Japan's USD 1.5 Billion Annual Hydrogen Investment Is Building Structural Market Demand

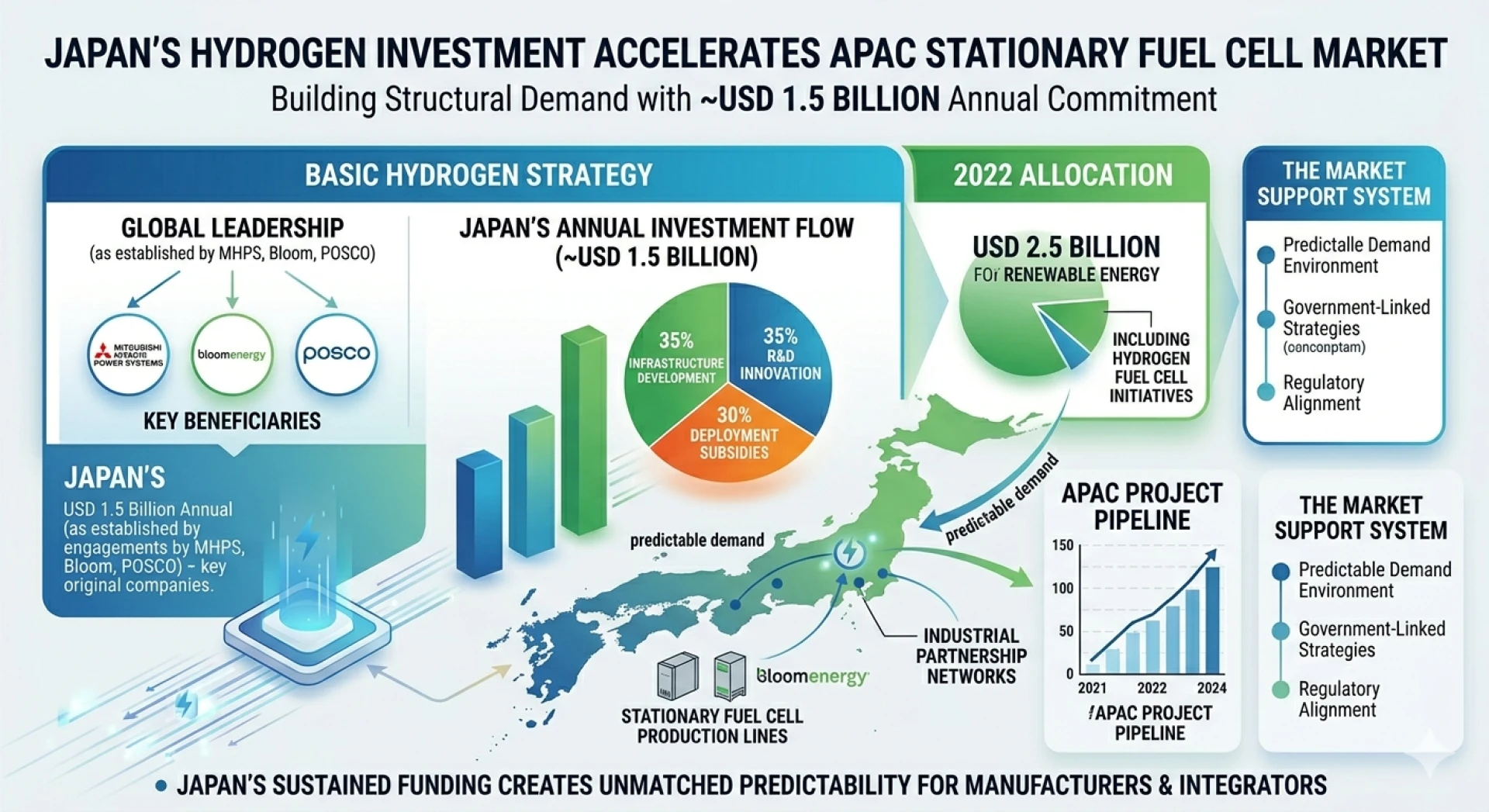

The single most commercially significant policy driver in the APAC stationary fuel cell market is Japan's sustained financial commitment to hydrogen energy infrastructure. With a projected annual investment of USD 1.5 billion through its Basic Hydrogen Strategy, Japan is creating a market support system that funds R&D, deployment subsidies, and infrastructure development simultaneously. In 2022, Japan allocated USD 2.5 billion specifically for renewable energy projects, including hydrogen fuel cell initiatives. This level of financial commitment creates a predictable demand environment for stationary fuel cell manufacturers and system integrators that few other clean energy segments in APAC can currently match.

According to Ken Research Analysis, government support for renewable energy transition is identified as the primary growth driver in the APAC stationary fuel cell market, with Japan's Ministry of Economy, Trade, and Industry and South Korea's Renewable Portfolio Standards creating the subsidy and tax credit frameworks that are converting policy ambition into active procurement.

Q: How is APAC stationary fuel cell industry size distributed across markets and product types?

The APAC Stationary Fuel Cell Industry Size is anchored by Japan and South Korea, which dominate through early adoption of hydrogen energy, substantial fuel cell R&D investment, and the presence of major fuel cell manufacturers within their domestic markets. Japan's strategic hydrogen economy push and South Korea's Hydrogen Economy Roadmap are the two primary frameworks driving this concentration. At the product type level, PEM (Proton Exchange Membrane) fuel cells hold the dominant share due to their high efficiency and suitability across the range from small residential systems to large-scale commercial power generation. SOFC, PAFC, and MCFC each serve more specialized application segments, with SOFC gaining share in industrial applications and PAFC maintaining relevance in utility-scale deployments.

Commercial Sector Adoption Is Leading Stationary Fuel Cell Deployment Across APAC

The commercial sector dominates stationary fuel cell adoption across APAC. Data centers, hospitals, and office buildings are the primary commercial adopters, selecting fuel cells to ensure continuous power supply while reducing carbon footprint. These applications are particularly well-suited to stationary fuel cells because they require reliable baseline power around the clock, cannot tolerate grid interruptions, and operate under sustainability mandates from both regulators and corporate governance frameworks. The fuel cell's ability to provide both electricity and heat through combined heat and power (CHP) configurations further strengthens its commercial value proposition, as it addresses both power reliability and energy efficiency requirements simultaneously.

Q: Where do the clearest APAC stationary fuel cell sector opportunities concentrate across geographies and end-uses?

The strongest APAC Stationary Fuel Cell Sector Opportunities are visible across three categories. First, residential micro-CHP expansion: Japan had over 400,000 households using Ene-Farm micro-CHP fuel cells by the end of 2023, demonstrating that residential fuel cell adoption can reach meaningful scale when supported by policy and product maturity. This creates a blueprint for scaling residential adoption in South Korea and eventually China. Second, industrial backup power: China's industrial sector had over 300 MW of stationary fuel cell installed capacity in 2023, demonstrating active deployment at industrial scale. Third, energy se curity investment: as APAC governments prioritize energy independence and grid resilience, stationary fuel cells are increasingly positioned as infrastructure assets rather than efficiency tools alone.

PEM Fuel Cells Lead the Product Mix Through Efficiency and Application Versatility

PEM fuel cells hold the dominant product type position in the APAC stationary fuel cell market because they combine high efficiency with the widest application range. From small residential Ene-Farm systems in Japan to large-scale commercial backup power installations, PEM technology scales across the deployment spectrum more effectively than any other fuel cell type. The increasing demand for decentralized energy systems, where power generation is distributed closer to end-users rather than concentrated in large central facilities, further propels PEM growth. Decentralized energy models reduce transmission loss, improve energy security, and align with both urban planning preferences and corporate sustainability strategies in Japan, South Korea, and increasingly China.

Product segmentation data from Ken Research Insights, confirms that PEM fuel cells hold the dominant market share in the APAC stationary fuel cell market, with their versatility across residential to commercial applications and the growing demand for decentralized energy systems driving their structural leadership position.

Conclusion

The APAC stationary fuel cell market's valuation of USD 1.30 billion reflects a market that has moved well past the demonstration phase into active commercial deployment backed by sustained government investment. Japan's USD 1.5 billion annual hydrogen commitment and South Korea's hydrogen economy framework are the two most reliable demand anchors in the near term. The commercial sector leads adoption. Residential micro-CHP is scaling. Industrial backup power is growing. PEM technology dominates the product mix. For operators and investors evaluating this market, the opportunities are multi-sectoral and geographically diverse, with Japan and South Korea offering near-term commercial certainty and China and Southeast Asia offering longer-horizon scale potential.