The global antibiotics API market is entering a period of structural instability, driven by geopolitical fragmentation, regulatory divergence, and the collapse of economic incentives for new antibiotic development. Companies that fail to reconfigure their sourcing strategies now risk supply disruptions, margin erosion, and regulatory non-compliance within the next 18 to 24 months.

Request Report Sample: https://marketmindsadvisory.com/request-sample/?report_id=8255

Why This Market Shift Matters Now

For decades, the antibiotics API market operated on a simple logic: consolidate production in low-cost geographies, optimize for scale, and compete on price. That model is breaking. Recent supply shocks, quality failures at major manufacturing hubs, and accelerating regulatory scrutiny have exposed the fragility of concentrated supply chains. At the same time, antimicrobial resistance (AMR) is escalating faster than new drug pipelines can respond, creating a paradox where demand for effective antibiotics is rising while commercial incentives to produce them are collapsing.

This is not a distant threat. Pharmaceutical companies are already experiencing longer lead times, quality variability, and price volatility for critical beta-lactam and fluoroquinolone APIs. Regulators in the US and EU are tightening environmental discharge standards for API manufacturing, effectively disqualifying suppliers who cannot meet new compliance thresholds. Meanwhile, governments are beginning to intervene directly in antibiotic supply chains through strategic stockpiling and domestic production mandates.

The companies that recognize this as a strategic inflection point—not just a procurement challenge—will gain significant competitive advantage. Those that treat it as business-as-usual will find themselves scrambling for supply, paying premium prices, and facing regulatory delays.

Structural Shifts Driving the Market

Geopolitical Fragmentation Is Forcing Supply Chain Redesign

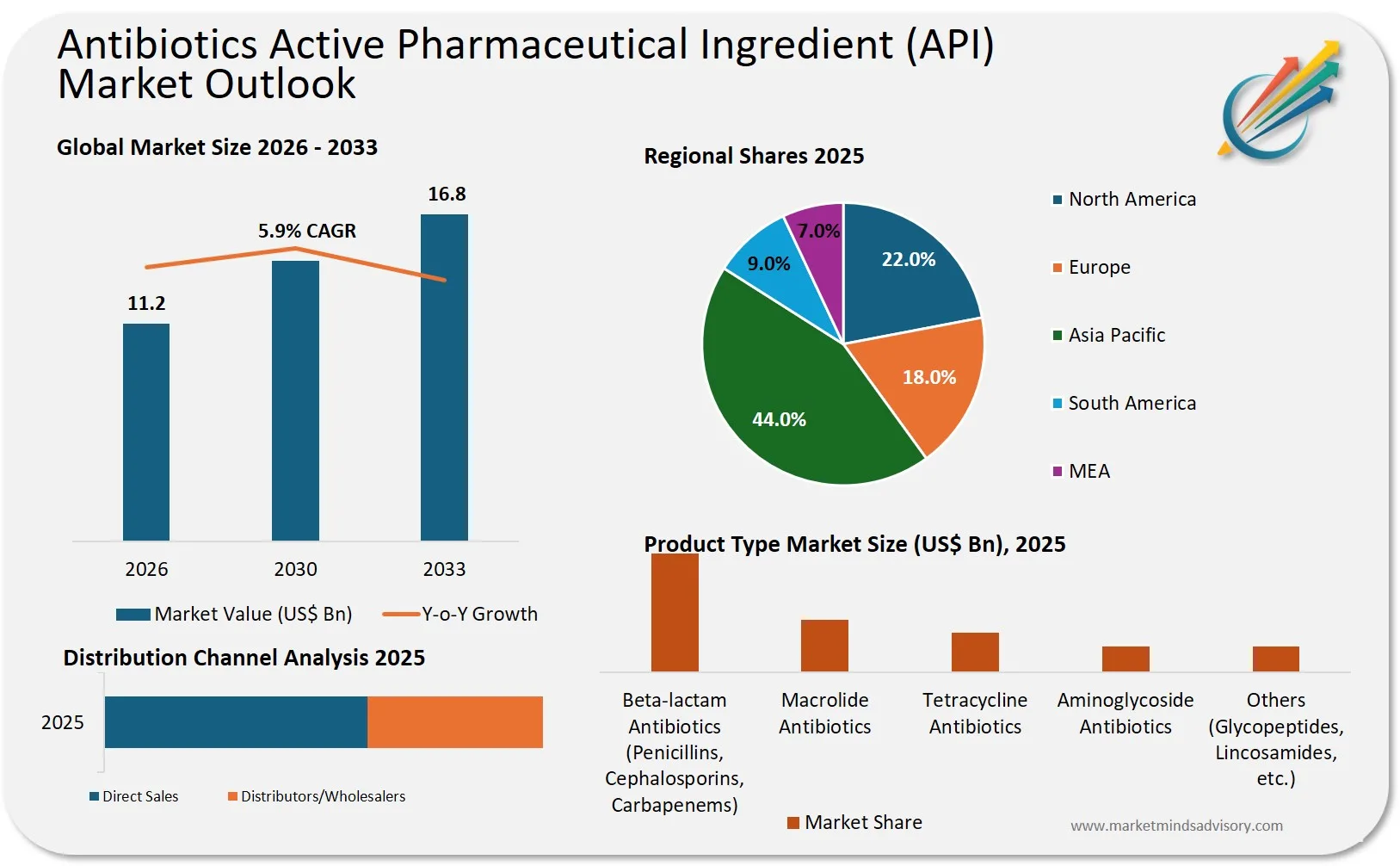

The antibiotics API market has long been dominated by manufacturers in China and India, which together account for the majority of global production. However, rising geopolitical tensions, export restrictions, and national security concerns are prompting Western governments to reduce dependency on these sources. The US BIOSECURE Act and similar European initiatives are creating pressure to diversify or reshore critical API production. This is not a theoretical policy discussion—it is already influencing procurement decisions at major pharmaceutical companies and creating openings for manufacturers in Eastern Europe, Latin America, and Southeast Asia.

Regulatory Pressure Is Redefining Supplier Viability

Environmental regulations are emerging as a critical filter for API suppliers. The EU’s updated Good Manufacturing Practice (GMP) guidelines now include stringent requirements for antibiotic manufacturing effluent, targeting antimicrobial residues that contribute to resistance development. Suppliers unable to invest in advanced wastewater treatment and environmental controls are being delisted by major buyers. This is creating a two-tier market: compliant suppliers who can command premium pricing, and non-compliant suppliers facing shrinking customer bases and regulatory exclusion.

Economic Incentives Are Misaligned With Public Health Needs

The antibiotics market suffers from a fundamental economic problem: the drugs that are most needed (novel antibiotics for resistant infections) are the least profitable. Payers and health systems deliberately restrict use of new antibiotics to preserve their effectiveness, which destroys the commercial case for development. As a result, multiple pharmaceutical companies have exited antibiotic R&D, and several specialized antibiotic developers have filed for bankruptcy despite having FDA-approved products. This is creating a dangerous gap between clinical need and commercial supply, with implications for API demand patterns and pricing structures.

Where the Real Opportunity Lies

The highest-value opportunities in the antibiotics API market are not in volume growth—they are in strategic positioning around supply security, regulatory compliance, and specialty segments.

Beta-lactam APIs, particularly those used in hospital settings for serious infections, represent a critical supply category where quality, reliability, and regulatory compliance matter more than price. Companies that can demonstrate consistent quality, environmental compliance, and supply continuity are gaining preferred supplier status and long-term contracts with major pharmaceutical companies.

Specialty and narrow-spectrum antibiotics are emerging as a distinct segment. As AMR concerns grow, there is increasing clinical and regulatory interest in antibiotics that target specific pathogens rather than broad-spectrum agents. APIs for these products command higher margins and face less price pressure, but require more sophisticated manufacturing capabilities and regulatory expertise.

Geographically diversified production capacity is becoming a competitive differentiator. Pharmaceutical companies are willing to pay premiums for suppliers with manufacturing footprints outside traditional hubs, particularly in regions with strong regulatory frameworks and political stability. This is creating opportunities for API manufacturers in the EU, US, and select emerging markets to capture share despite higher cost structures.

Browse the Complete Report: https://marketmindsadvisory.com/antibiotics-active-pharmaceutical-ingredient-api-market/

Competitive or Strategic Shift

The antibiotics API market is transitioning from a commodity business to a strategically managed supply category. Historically, purchasing decisions were driven almost entirely by price and volume capacity. That is changing rapidly. Pharmaceutical companies are now evaluating suppliers based on a broader set of criteria: regulatory compliance track record, environmental sustainability, geopolitical risk exposure, financial stability, and willingness to enter into long-term supply agreements.

This shift is creating a bifurcation in the supplier base. Large, vertically integrated manufacturers with strong quality systems and regulatory compliance are consolidating relationships with major pharmaceutical companies. Smaller, price-focused suppliers are being squeezed out or relegated to secondary status. The middle ground is disappearing.

At the same time, the threat of commoditization remains real for suppliers who cannot differentiate on quality, compliance, or supply security. As more manufacturers achieve baseline GMP compliance and environmental standards, the competitive advantage will shift to those who can offer integrated solutions—such as API supply bundled with regulatory support, formulation development assistance, or inventory management services.

The Cost of Delayed Action

Companies that postpone strategic decisions around antibiotics API sourcing and supply chain configuration will face compounding consequences:

- Supply disruptions become more likely as geopolitical tensions escalate and regulatory enforcement intensifies, leading to production delays and revenue loss

- Margin compression accelerates as scrambling for alternative suppliers forces acceptance of premium pricing without corresponding product differentiation

- Regulatory compliance failures increase in probability as legacy suppliers fail to meet evolving environmental and quality standards, triggering costly remediation and potential product recalls

- Strategic optionality narrows as preferred suppliers lock into long-term agreements with competitors, leaving late movers with limited choices and weaker negotiating positions

- Reputational damage from supply failures or association with non-compliant suppliers becomes harder to reverse in an environment of heightened scrutiny

The window for proactive repositioning is closing. Suppliers and pharmaceutical companies that act now can negotiate favorable terms, secure capacity, and build resilient supply chains. Those that wait will be forced into reactive, expensive solutions.

What This Means for Decision-Makers

For Pharmaceutical Companies and Generic Manufacturers

Your antibiotics API sourcing strategy needs immediate review. Conduct a comprehensive risk assessment of your current supplier base, evaluating geopolitical exposure, regulatory compliance status, and financial stability. Identify critical APIs where you have single-source dependencies or concentration in high-risk geographies. Begin qualifying alternative suppliers now, even if it means accepting higher costs in the short term. Consider entering into long-term supply agreements with strategically important suppliers to secure capacity and pricing. Integrate environmental compliance and AMR stewardship into your supplier selection criteria—these will increasingly influence regulatory approvals and market access.

For API Manufacturers and Chemical Companies

The competitive landscape is being redrawn. If you are currently competing primarily on price, that position is becoming untenable. Invest in regulatory compliance infrastructure, particularly around environmental controls and quality systems. Pursue certifications and audits from US FDA and EU regulatory authorities to differentiate your offering. Consider geographic expansion or partnerships to diversify your manufacturing footprint. Develop capabilities in specialty and narrow-spectrum antibiotic APIs where margins are more sustainable. Build direct relationships with pharmaceutical company procurement and quality teams rather than relying solely on distributors or trading companies.

For Investors and Capital Allocators

The antibiotics API market presents a complex investment thesis. On one hand, structural demand is stable and regulatory barriers to entry are high. On the other, pricing pressure and economic disincentives create margin challenges. The most attractive opportunities lie in companies that have achieved regulatory differentiation, geographic diversification, or vertical integration. Be cautious of pure-play commodity API manufacturers with concentrated customer bases or exposure to regulatory risk. Look for companies investing in environmental compliance and quality infrastructure—these are likely to gain share as standards tighten. Consider the strategic value of API manufacturing assets in the context of broader pharmaceutical supply chain resilience trends.

For Policymakers and Regulators

Current market dynamics are creating a dangerous misalignment between public health needs and commercial incentives. Regulatory interventions focused solely on quality and environmental standards, while necessary, may inadvertently reduce supply and increase costs without addressing the underlying economic problem. Consider complementary policy mechanisms such as volume guarantees, milestone payments for maintaining production capacity, or tax incentives for domestic API manufacturing. Coordinate internationally on regulatory standards to avoid fragmentation that increases compliance costs without improving outcomes. Recognize that antibiotics are a strategic asset requiring active market stewardship, not just passive regulation.

The antibiotics API market is at a critical juncture where strategic foresight will separate winners from those left managing perpetual crisis.

The next 24 months will determine which companies secure resilient supply chains and which face chronic instability. The data is clear, the risks are material, and the window for proactive action is narrowing. Decision-makers who treat this as a strategic priority rather than a procurement issue will position their organizations for sustained competitive advantage in an increasingly complex and fragmented market.

About Company

At Market Minds, we’re more than just consultants—we’re partners in your journey to growth and success. We combine deep industry expertise with cutting-edge research to uncover insights that truly matter, helping you navigate challenges and seize opportunities with confidence. Whether it’s adapting to market shifts, exploring new revenue streams, or staying ahead of emerging trends, our focus is always on delivering tailored solutions that drive real results. With us, you’re not just getting advice—you’re gaining a trusted team dedicated to your success, every step of the way.

Contact Us

Market Minds Advisory

86 Great Portland Street, Mayfair,

London, W1W7FG,

England, United Kingdom

Phone: +44 020 3807 7725

Email: [email protected]

Website: https://marketmindsadvisory.com/