Distressed property owners face a stacked deck: mounting repairs, looming mortgages, complicated liens, and the emotional drain of a home they can’t maintain. For many, listing on the open market isn’t an attractive option. That’s where investors and cash buyers step in—offering speed, certainty, and practical solutions that traditional buyers and agents often can’t match. Brands like Pennington Real Estate Investments specialize in creating win-win solutions for sellers who need relief fast. This article examines why those selling under pressure increasingly prefer cash transactions and how sellers can make the smartest choice.

What counts as a “distressed” property?

A distressed property can mean different things—physical deterioration, tax or mortgage delinquency, probate or estate complications, or properties burdened with code violations or liens. The common thread is urgency: the owner needs to move quickly, or the property will cost more to hold than it’s worth.

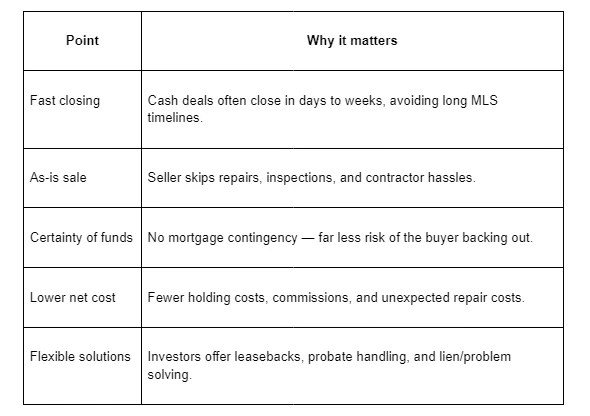

1. Speed and certainty beat the traditional market

One of the chief advantages cash buyers offer is a dramatically faster transaction timeline. Traditional sales can take 45–90 days (or longer) with showings, contingencies, and mortgage underwriting. Cash investors can often close in days or a few weeks because they don’t wait on lender approvals. For sellers racing against foreclosure, handling an estate, or eager to stop leaking money into repairs and taxes, that certainty is priceless.

2. “As-is” sales eliminate repair headaches and costs

Distressed homes often need significant work. Listing a property typically triggers inspection demands, repair negotiations, or credits that delay the sale and reduce proceeds. Cash buyers commonly purchase properties “as-is,” absorbing the cost and responsibility of rehab. That removes uncertainty for sellers and simplifies the process—no contractor calls, no inspection renegotiations, no surprise repair bills.

3. Lower transactional friction and fewer costs

Traditional sales involve agent commissions, buyer financing contingencies, title issues, and holdover costs while a home sits on the market. Investors who specialize in troubled homes understand how to clear title issues or negotiate around liens and pay fewer transactional fees. While cash offers may sometimes be below peak market value, the net proceeds after commissions, repairs, and holding costs can be competitive—and often preferable when time or stress is factored in.

4. Creative solutions for complicated situations

Investors bring flexibility that many retail buyers cannot. They can structure deals to help sellers who need time to relocate, pay off a mortgage, or divide proceeds among heirs. Options can include leasebacks, subject-to financing, or staged closings for complex estates. For someone unfamiliar with real estate legalities, having an investor experienced in these solutions can make a messy situation manageable.

5. Expertise and a built-in remediation network

Professional cash buyers are not just check writers; they’re project managers. They know local permitting, contractor rates, and resale channels. That network shortens the time between purchase and profit and reduces hidden rehab surprises. Sellers benefit indirectly: the investor’s efficiency often results in a smoother closing and fewer last-minute complications.

6. Risk mitigation—avoid the “buyer dropout”

One of the common frustrations in traditional listings is the buyer who backs out after inspections or after financing falls through. Cash purchases dramatically reduce this risk. Because funding is already secured, sellers are far less likely to be blindsided by a failed mortgage contingency or a paused escrow—giving a reliable way to move on.

7. When selling fast is also financially smart

A quick sale may seem like accepting less money, but in distressed situations, the true cost of delay can be substantial: mortgage arrears, utility bills, insurance, property taxes, and theft or vandalism on vacant properties. Cash transactions remove these continuing liabilities immediately. For a seller under pressure, a slightly reduced price today can lead to a better financial outcome than waiting for a higher offer that may never appear.

How to choose the right cash buyer

Not all cash buyers are equal. Prioritize transparency and local reputation. A few tips:

- Ask for references and recent closings.

- Verify proof of funds before considering any offer seriously.

- Request a clear, written breakdown of fees and closing costs.

- Confirm how the buyer will handle title, liens, or code violations.

- Avoid buyers who push you for an immediate signature or refuse to put terms in writing.

If you’re evaluating professional options, compare local property buyers services with independent investors to find the best fit for your timeline and goals.

Typical process when you decide to sell to a cash buyer

- Initial contact and property overview (photos, basic facts).

- Buyer visits the property or reviews documentation.

- Offer presented — often a firm, no-contingency price.

- Agreement and title search; buyer provides proof of funds.

- Closing — commonly within a week to 30 days.

If your priority is simply to sell distressed property fast and cleanly, this streamlined process removes many hurdles of the MLS route.

Red flags to watch for

- Unwillingness to provide proof of funds.

- Pressure tactics to sign immediately.

- Vague terms or refusal to use a licensed title company/attorney.

- Offers significantly below market with no explanation.

Always consult a real estate attorney or trusted advisor for complex title issues or if there’s confusion about liens, probate, or tax warrants.

Real-world scenarios where investors shine

- An inherited house with multiple beneficiaries who want a clean split without rehab hassle.

- A homeowner facing foreclosure who needs funds fast to avoid credit damage.

- A rental property owner is overwhelmed by repairs and chronic vacancies.

In each case, investors provide quick liquidity and assume the burden of getting the property back to marketable condition.

Speed, Simplicity, and Certainty

For many distressed property owners, the investor advantage is straightforward: a faster, less stressful route to a clean exit. Cash buyers bring certainty where the traditional market brings delays and negotiation headaches. That doesn’t mean every seller should accept the first cash offer—due diligence matters—but for those weighed down by repairs, liens, or tight timelines, working with reputable professionals like Pennington Real Estate Investments can be the clearest path forward.

If you’re considering your options, weigh the cost of time and stress against a firm cash offer. When urgency, simplicity, and a guaranteed close are priorities, investors often provide the outcome distressed owners need.

FAQS (Frequently Asked Questions)

Q1: How quickly can a cash sale close?

Typically, within 7–30 days; some buyers can close in just a few days if the paperwork is ready.

Q2: Will I get less money selling to a cash buyer?

Cash offers may be below retail, but net proceeds can be better once you factor in repairs, commissions, and holding costs.

Q3: How do I verify a cash buyer is legitimate?

Ask for proof of funds, references, and a written offer, and use a licensed title company or attorney at closing.

Q4: Do I need an agent or attorney?

Not required, but an attorney is wise for complex title, lien, or probate issues; an agent can help if you want to compare offers.

Q5: Can investors buy homes with liens, code violations, or foreclosure threats?

Yes, many investors specialize in resolving liens, code issues, and foreclosure scenarios; always confirm details in writing.