You spent decades saving and investing. Now the real challenge begins: turning your nest egg into a steady paycheck without giving too much away in taxes. The way you pull money from different accounts each year is one of the most powerful (and misunderstood) retirement income strategies you have.

Get your withdrawal order wrong, and you can pay more tax than you need to, trigger Medicare surcharges, and face big required minimum distributions (RMDs) later. Get it right, and you may stretch your savings, reduce stress, and give yourself more freedom in retirement.

Why expert guidance matters

Many retirees discover, often the hard way, that “I’ll just take money when I need it” is not a plan. This is where working with a seasoned financial advisor for retirement, such as Tull Financial Group, can make a huge difference. An advisor helps you choose which account pays for each year of spending so you keep more of what you’ve already earned.

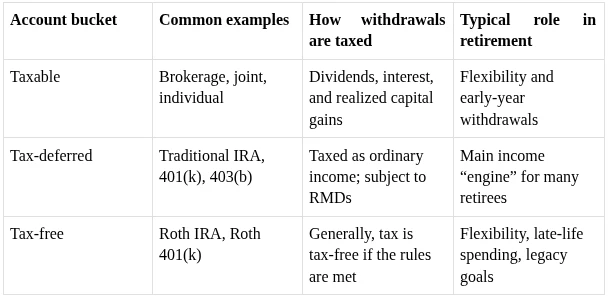

Understanding your three main account buckets

Before you decide on any sequence, you need to know what you are sequencing. Most retirees have three broad types of accounts:

- Taxable accounts (brokerage, joint, individual accounts)

- Tax-deferred accounts (traditional 401(k), 403(b), traditional IRA)

- Tax-free accounts (Roth 401(k), Roth IRA, some HSAs when used for healthcare)

These buckets have different tax rules, and that is why the withdrawal order matters so much.

Table: How your retirement buckets are taxed

Once you reach age 73, the IRS generally requires annual withdrawals (RMDs) from most tax-deferred accounts, whether you need the cash or not. (IRS)

Do you know?

You can use official IRS Required Minimum Distribution FAQs and RMD worksheets to estimate how much you must withdraw each year from tax-deferred accounts. (IRS)

From rules to action: tax-efficient withdrawal strategies

Research and real-world experience show that a thoughtful sequence of withdrawals — what professionals call tax-efficient withdrawal strategies — can increase the amount you get to spend over your lifetime. Instead of draining one bucket completely and then moving to the next, a smarter approach blends withdrawals across accounts to keep your taxable income in a comfortable range.

A common default “ladder” looks like this:

- Spend interest, dividends, and any guaranteed income first.

- Use taxable accounts to fill the gap.

- Add tax-deferred withdrawals up to the top of your target tax bracket.

- Preserve Roth savings for flexibility and future tax control.

Where retirement tax planning changes the game

Most people think of taxes once a year, at filing time. But in retirement, smart retirement tax planning means looking forward, not backward. Your questions shift from “What do I owe?” to:

- Which account should fund my spending this year?

- How can I keep my taxable income in a stable range over time?

- Can I use today’s lower tax bracket to reduce future tax bills?

Pro tip: Don’t view your tax return in isolation. Share it with your advisor every year. It acts like an “X-ray” of your income sources and deductions and helps your planner design smarter, more coordinated withdrawals for the coming year.

Designing tax-efficient retirement income you can live with

You don’t just want tax savings; you want a steady, reliable income. Thoughtfully designed tax-efficient retirement income balances three goals:

- Cover your monthly spending with confidence.

- Keep your tax bill as low and predictable as possible.

- Protect your savings so they last longer through longer lifespans and rising costs.

A practical, flexible approach often looks like this:

- Use pensions, annuities, and Social Security as your base.

- Fill the remaining need from a mix of taxable and tax-deferred accounts.

- Use Roth accounts strategically when other income spikes (for example, after selling a property).

To estimate how Social Security fits into your plan, you can try the official Social Security benefit calculators. They show how claiming at 62, full retirement age, or 70 changes your monthly benefit and your need to withdraw from investments. (Social Security)

How Roth conversions can smooth future taxes

The years between retirement and your first RMD can be “low-tax” years. During this window, some retirees choose to convert portions of their pre-tax IRA or 401(k) into a Roth account:

- You pay tax on the conversion now.

- Future growth in the Roth can be withdrawn tax-free (if rules are met).

- Your future RMDs may shrink because your traditional balance is smaller.

Note: Roth conversions are powerful, but they are not one-size-fits-all. Converting too much in one year can push you into a higher tax bracket or affect Medicare costs. This is another area where coordinated advice matters.

Role of a retirement financial planner in drawdown decisions

A seasoned retirement financial planner helps turn complex rules into a simple, usable plan. With Tull Financial Group, that often includes:

- Mapping all account balances, tax status, and expected cash flows.

- Projecting income and taxes under different withdrawal orders.

- Coordinating Social Security timing with portfolio withdrawals.

- Stress test your plan against market drops and rising inflation.

Instead of guessing which account to tap, you follow a written, flexible playbook that gets updated every year.

Linking withdrawals to your lifestyle timeline

Your life in retirement doesn’t stand still. Many people move through three broad stages:

- “Go-go” years: travel, hobbies, home projects.

- “Slow-go” years: more time at home, moderate spending.

- “No-go” years: potential healthcare and support costs dominate.

Tull Financial Group often encourages clients to think about which stage they’re in and how that shapes the withdrawal plan. Spending may be higher at first and then shift toward healthcare later. Your withdrawal sequence can mirror this pattern.

Planning forward with structured retirement planning

At some point, you want clarity, not just information. Detailed retirement planning with Tull Financial Group pulls everything together:

- Your savings, pensions, and Social Security.

- Your tax picture today and projected into the future.

- Your wishes for travel, family, giving, and legacy.

From there, your advisor helps design a tax-smart withdrawal strategy that fits your goals, and then walks with you year by year as life unfolds.

Wrap Up

Sequencing withdrawals is one of the most overlooked levers in retirement. Instead of pulling money “as needed,” you:

- Understand how each account bucket is taxed.

- Use research-backed ideas about tax-efficient sequences.

- Match your withdrawal plan to your lifestyle stages.

- Adjust every year as markets, laws, and life circumstances change.

The result can be lower lifetime taxes, smoother income, and more confidence that your money will last as long as you do.

Key takeaways

- Withdrawal order can matter as much as investment choice in retirement.

- Blending taxable, tax-deferred, and Roth withdrawals often beats draining one bucket at a time.

- RMD rules at age 73 make it critical to plan rather than react at the last minute.

- Tools from the IRS, Social Security, and the SEC give helpful data, but a personalized plan turns that data into action.

- A trusted advisor can help you adjust as tax laws and your life evolve.

FAQs

1. When should I start planning my withdrawal sequence?

Ideally, you begin five to ten years before retirement. That gives you time to decide where to save (taxable, pre-tax, Roth), think about Social Security timing, and model different withdrawal paths before you actually need the income.

2. How often should I review my withdrawal plan?

Most retirees benefit from a full review at least once a year. You should also revisit the plan whenever you experience a major life event: a big market change, a home sale, an inheritance, or a significant health event.

3. Can I handle this on my own with calculators and spreadsheets?

You can get a useful start with government tools like the IRS RMD resources and Social Security calculators, plus the SEC’s retirement planning guides. But many people find it reassuring to partner with a firm like Tull Financial Group to coordinate investments, taxes, and real-life goals so they are not making high-stakes decisions alone.