For lenders, technology choices directly influence speed, compliance, and customer experience. Two core systems often mentioned in this context are the Loan Origination System (LOS) and the Loan Management System (LMS). While the terms are sometimes used interchangeably, they serve very different purposes in the lending lifecycle. Understanding the distinction helps banks and NBFCs avoid inefficiencies, select the right technology stack, and ensure better risk and operational control.

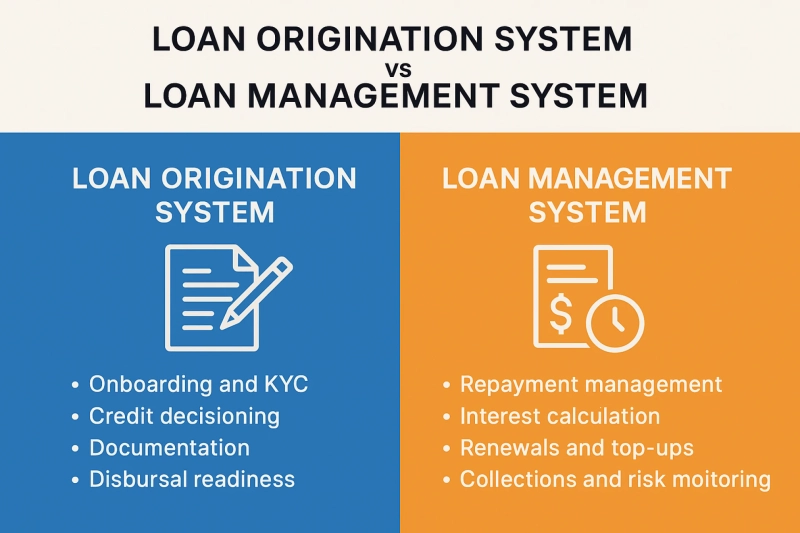

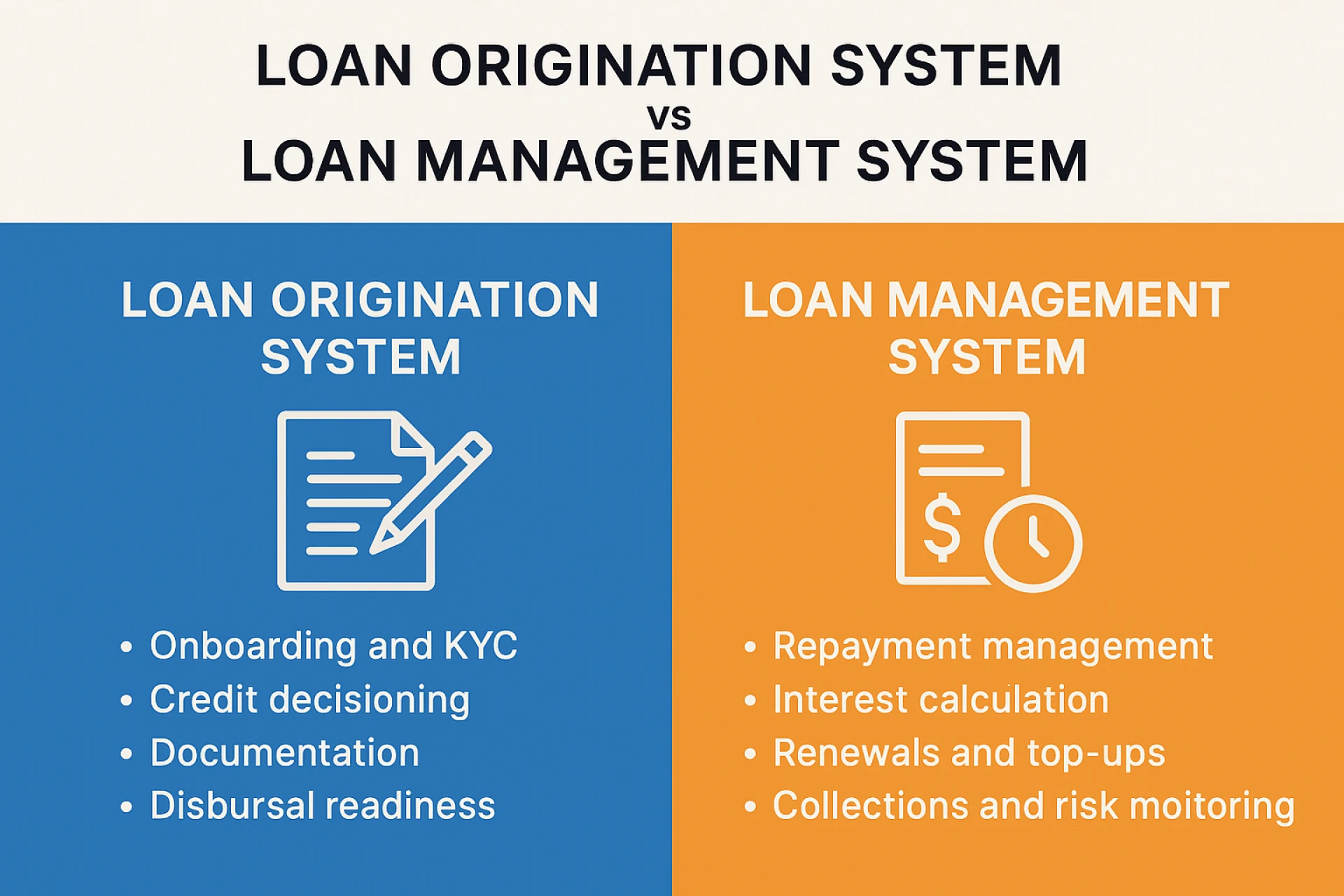

What is a Loan Origination System?

A Loan Origination System (LOS) manages everything from the moment a borrower applies for credit until the loan is sanctioned and disbursed. It is designed to streamline and automate the origination journey across different loan products.

Key functions of a Loan Origination System include:

- Digital onboarding and KYC/KYB: Collecting borrower data, verifying identities, and validating compliance requirements.

- Data ingestion: Integrating external sources like GST, bank statements, and credit bureau reports to assess borrower eligibility.

- Credit decisioning: Applying business rules, scorecards, and underwriting logic to arrive at approval or rejection.

- Limit and documentation setup: Finalizing drawing power, limits, and generating digital loan agreements.

- Disbursal readiness: Ensuring compliance, approvals, and system checks before releasing funds.

In short, a LOS is built for speed, accuracy, and automation at the front end of the lending process.

What is a Loan Management System?

A Loan Management System (LMS), by contrast, takes over once a loan has been sanctioned and disbursed. Its role is to manage the loan through its active lifecycle—right until closure.

Key functions of a Loan Management System include:

- Repayment management: Scheduling EMIs or flexible repayment structures such as daily, weekly, or milestone-linked payments.

- Interest and fee calculations: Automating accruals, charges, and adjustments across different loan products.

- Renewals and top-ups: Handling extensions, restructuring, and repeat financing.

- Accounting and reconciliation: Ensuring ledgers are updated in sync with core banking or ERP systems.

- Collections and risk monitoring: Tracking overdue accounts, generating alerts, and integrating with collection workflows.

- Audit and compliance: Maintaining role-based controls, audit trails, and regulatory reporting.

An LMS is therefore built for control, accuracy, and compliance at the back end of the lending process.

Loan Origination System vs Loan Management System: Key Differences

Although both systems are integral to lending, their purposes differ across five key dimensions:

AspectLoan Origination System (LOS)Loan Management System (LMS)Stage of UsePre-disbursement (application to sanction)Post-disbursement (sanction to closure)Primary GoalFaster, more accurate credit decisioningEffective servicing and monitoring of loansKey UsersSales, credit, underwriting teamsOperations, finance, collections teamsCore FunctionsOnboarding, KYC, credit evaluation, approvals, documentationRepayment tracking, renewals, restructuring, collections, complianceValue DeliveredReduced turnaround time, improved customer experience, better risk-based decisioningImproved operational efficiency, lower delinquency, stronger governance

Why the Distinction Matters for Lenders

Many lenders attempt to manage the entire lifecycle on a single system, but this often leads to operational inefficiencies. A Loan Origination System needs flexibility to adapt to evolving credit policies, regulatory updates, and new product launches. A Loan Management System, on the other hand, requires stability, precision in accounting, and robust compliance features.

Without clear separation, lenders may face:

- Longer turnaround times due to manual handovers and workarounds.

- Data inconsistencies between origination and servicing stages.

- Compliance risks if audit trails and reporting are not seamlessly maintained.

A well-defined LOS and LMS setup ensures smooth handovers, better tracking, and end-to-end visibility across the borrower lifecycle.

Technology Trends Shaping LOS and LMS

Indian banks and NBFCs are now looking at platforms that are:

- No-code configurable: Allowing business users to change workflows and credit logic without IT bottlenecks.

- Integration-ready: Connecting with GST, PAN, bureaus, bank APIs, and ERP systems seamlessly.

- Audit and compliance-first: Embedding maker-checker controls, logs, and reporting by design.

- Product-agnostic: Supporting MSME lending, consumer finance, supply chain finance, and more on a single platform.

Platforms like CredAcc combine both Loan Origination System and Loan Management System capabilities into a unified, configurable infrastructure. This enables lenders to move quickly on product launches while maintaining lifecycle control, audit readiness, and regulatory compliance.

Conclusion

The difference between a Loan Origination System and a Loan Management System lies in where they operate within the lending lifecycle. LOS powers the journey from application to disbursal, while LMS manages the loan until closure. Both are essential, but they serve different goals—speed and customer experience on one hand, and compliance and operational efficiency on the other.

For Indian lenders facing rising borrower demand, tighter regulations, and the need for faster go-to-market, adopting robust LOS and LMS technology is no longer optional. With a partner like CredAcc, banks and NBFCs can deploy end-to-end digital lending systems that bring speed, compliance, and scale together.